Over the last few months, something has fundamentally changed in macroanalysis around the world. After lurking on the sidelines for years, without too much of policy implications, inflation is now beginning to inch towards the center stage.

With commodities’ price rise, supply bottlenecks and more, inflation finally is becoming a variable to reckon with. It is of even more importance given the rock-bottom yields in most of the developed world, and the need to forecast when the yields will finally inch up.

Unlike most other variables, inflation is not a simple one. There are various ways to look at it: actual inflation, inflation expectations and the central banks' view of inflation, among others. Not only that, the details of calculating inflation and how much of it is supply or demand-led; what is core inflation; how much is transitory (or not); what is the labour market indicating — the answers to all of these influence the reactions of both central banks and markets to this variable.

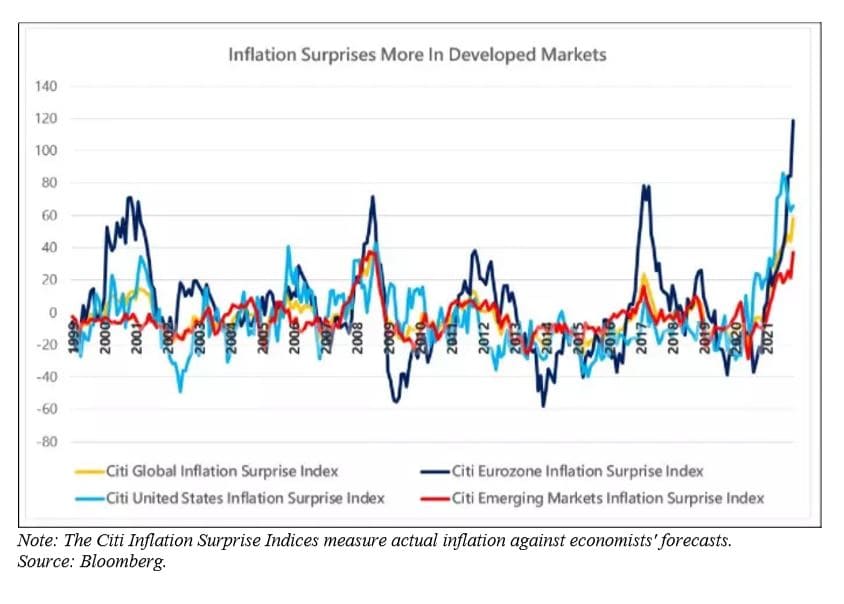

In this piece I have tried to give an overview of what is happening around the world, especially the West, and why. Inflation in the European Union (EU), for instance, is at the highest since records began in 1997. US core inflation is also the highest in 30 years. And, as discussed later, this has been a period where inflation surprises have been more in the developed economies rather than in the emerging ones — an unusual situation.

Inflation pinch for the US

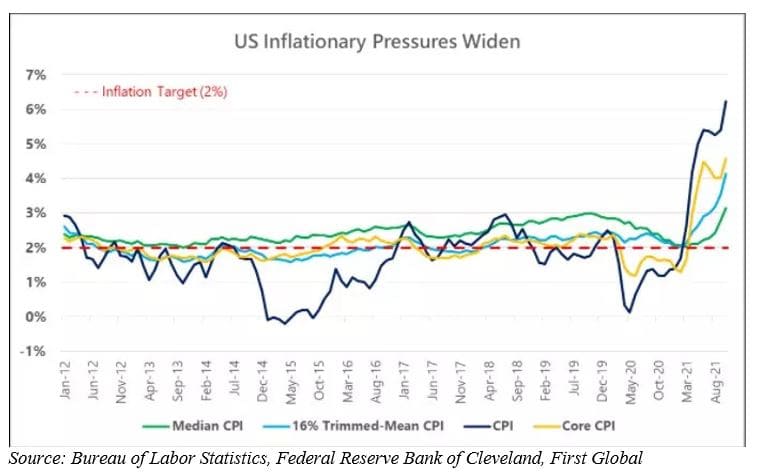

In the US, headline inflation Rate (Consumer Price Index or CPI) has surged to 6.2 per cent year-on-year (yoy), while core measure (excludes volatile food and fuel components) bounced to 4.6 per cent yoy, the fastest pace since 1990. Even after omitting outliers (small and large price changes) and focusing on the interior of the distribution of price changes, the median CPI (+3.1 per cent yoy) suggests inflationary pressures are omnipresent.

While a host of factors are responsible for the return of the inflation bogeyman, here is what we believe holds the key to understanding the dynamics of the situation:

Inflation sensitivity to Covid-19

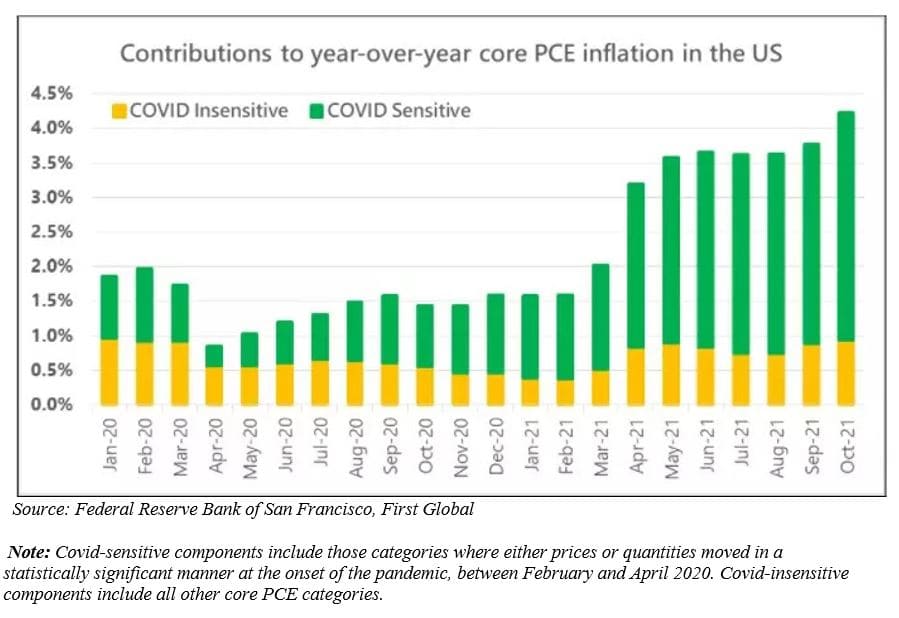

Apart from the well-known pandemic-induced excess demand for durable goods (over services), aided by pent-up savings and helicopter money (fiscal aid), persistent and underappreciated supply-side constraints have been a significant contributor to sticky inflation rate. Data show that 77 per cent of the 4.2 per cent yoy core inflation (personal consumption expenditure or PCE) in the US in October was due to Covid-sensitive goods and services.

Supply shortage spreads to the labour market

There is no dearth of indicators that show an extremely tight labour market in the post-pandemic world. While job openings in the US remain close to series highs of 10.4 million, it is the “quits rate” — people quitting or dropping out of jobs — that underscores the tightness in the labour market. The US Labor Department's monthly Job Openings and Labor Turnover Survey (JOLTS) showed that a record 4.4 million Americans quit their jobs in September, incentivised by record wage gains and other attractive terms offered by employers desperate for talent. The government handouts given earlier have also been a factor lowering consumer debt and, hence, decreasing the incentive to continue with an unsatisfactory job. As one would expect, the quit rate remained the highest in the Covid-sensitive sectors such as leisure and hospitality (6.4 per cent) and retail trade (4.4 per cent).

According to ManpowerGroup's latest quarterly survey, which includes 43 countries, mostly in Europe and North America, 69 per cent of the employers said they were having difficulty in filling employment positions — that is a 15-year high number. A Willis Towers Watson survey indicated that 70 per cent of the employers in the US expected hiring difficulties to persist in 2022 as well. 61 per cent admitted that even retaining employees was a challenge, up from a tepid 15 per cent last year. 75 per cent of the employers that flagged a budget increase next year (relative to projections) attributed it to tight labour market concerns.

A natural outcome of strong labour markets is rising wages. Comments by key central bank officials indicate that this is indeed one of the risk indicators that central banks have been monitoring to help them make decisions.

The latest data by BLS revealed that the employment cost index, a broad measure of wages and benefits in the US, rose 1.3 per cent in Q3, the biggest one-quarter jump since the index’s inception in 2001. Hourly wages rebounded 5.8 per cent yoy in October, the third-highest year-over-year wage growth since the early 1980s.

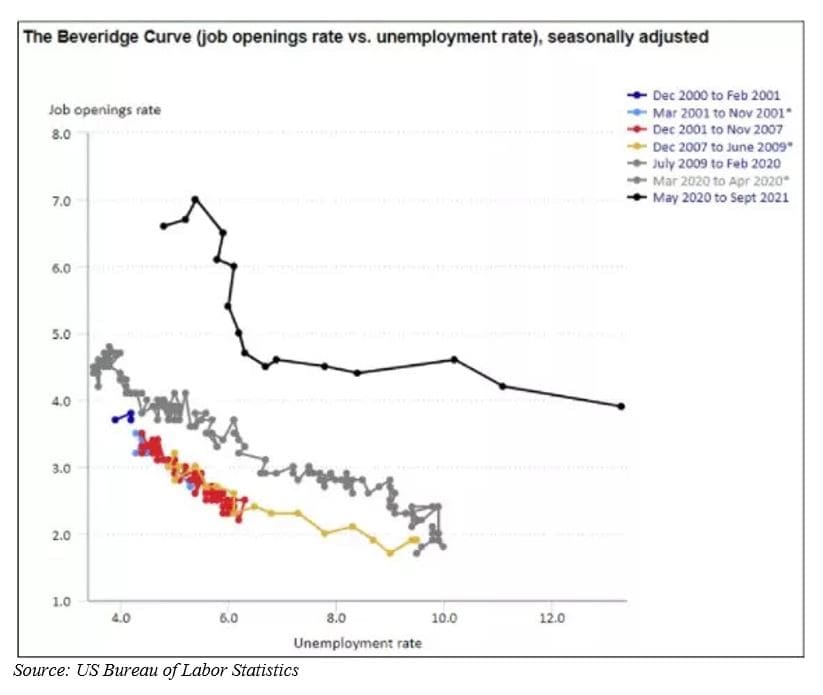

To be fair, wage growth has been tepid over the past few decades, so one could argue this is only a catch-up situation and that we’re not yet in a wage spiral. Nevertheless, it remains a consequential data point to track, given the peculiar developments in the so-called Beveridge Curve.

The Beveridge Curve captures the unemployment rate on the horizontal axis and the vacancy rate on the vertical axis. Pandemic data show a massive shift upward and to the right from pre-pandemic levels and a steep upward tilt once the recovery picked up speed in October 2020. Why the shift? Think skill-mismatch. If the matching process between workers and firms becomes less efficient, a given unemployment rate implies a higher job opening rate as is evident from the data cited above.

Different drivers locally, same outcome globally

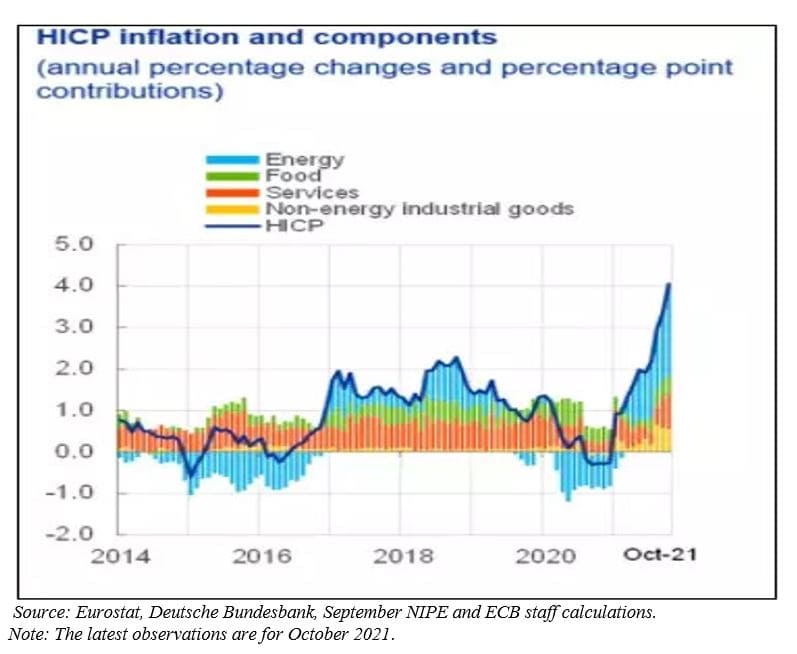

While the drivers of inflation might differ across regions (for example, food inflation may play a big role in EM baskets while housing costs may be a larger contributor for the US), inflation is undoubtedly a global phenomenon. Euro-area headline inflation rate surged to 4.9 per cent yoy in October (+2.6 per cent yoy for core, a two-decade high), a record for the era of the single currency and exceeded all forecasts.

However, to give credit where it is due, Europe has been facing an unprecedented power crisis. For example, Dutch TTF natural gas prices are up +400 per cent year-to-date, while French day-ahead power prices broke above €300 per MWh recently, one of the highest prices. Consequently, we witnessed production cuts across industrial establishments on the back of unsustainably high power prices. This made it unviable for companies to operate their factories and some utility firms were left asking for government bailouts. Hence, it would come as no surprise that more than 50 per cent of the rise in the Euro-area HICP inflation numbers are owed primarily to skyrocketing power prices.

Nevertheless, inflation is currently at three (3) times the target for major developed market economies. Although ubiquitous, inflation surprises have inarguably been more rampant in developed economies this time around than in emerging ones. No wonder, political pressure on central bankers is on the rise — be it from Germany's incoming chancellor Olaf Scholz or US President Joe Biden.

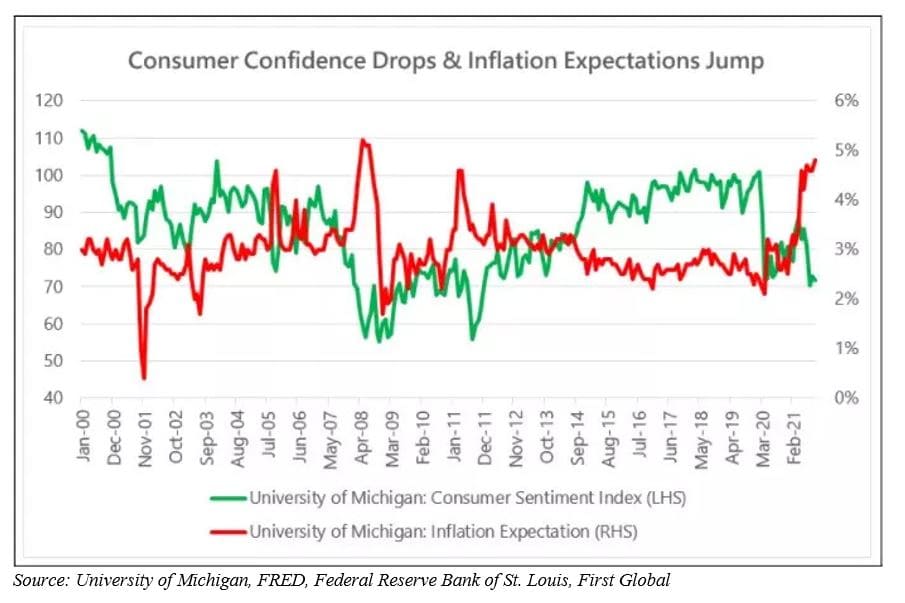

Sure, in the end, inflation could well turn out to be “transitory” as supply chains re-adjust, inventories build-up and demand normalises. However, if this transition period is protracted, the supply shock may inevitably morph into an “expectations shock” as consumers start to question the central bank’s credibility leading to a reflexive action or self-fulling prophecy where inflation spirals higher purely from the higher price expectations being built-in.

In our global fixed income portfolios, we have generally bet against the myth of inflation fallacy being “transitory” given the strong fiscal stimulus backdrop, complicated & prolonged supply chain issues, and a significant outward shift in the Beveridge curve which put incremental pressure on wages. This underpinned our short duration (underweight interest-rate sensitive bonds) and long credit positioning (floating-rate loans, high yield bonds). Now, finally, the central banks appear to be coming around to our view.

Throwing in the towel

Everyone in life has a risk manager. Central banks do too. At some point, the tap comes “enough is enough”. The risk managers here are the politicians. US Fed Chair Jerome Powell on November 30 officially retired the use of “transitory” to define inflation 2022, thus making inflation as the more likely variable to impact Fed policy, against the downside risk to employment. In short, making it more likely that the Fed would hike rates or tighten liquidity in order to control inflation instead of the other way around. Expectedly, this sparked a sharp sell-off from equities to commodities to bonds — highlighting the symptoms of liquidity withdrawals amid rampant inflationary pressure.

Looking forward: asymmetric policy response

Markets are in a quandary. Absent new variant concerns, cases were already spiking across Europe, the inflation rate was increasing, and tightening financial conditions were being priced in. Now that we have a new variant, the scaling back of implied accommodation removal is not going to be symmetric in nature. This is evident from market pricing, which still implies a 25 basis point hike for as early as June 2022 by the US Federal Reserve. Given this tricky scenario, it is more important than ever to dynamically adjust positions with a focus on protecting capital.

The number of variables that both central banks as well as investors and market participants have to juggle for their decision-making are only increasing, with a number of uncertainties being thrown into the equation. Vigilance in investment policies remains the key.

(A version of this article first appeared in The Economic Times)

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side, super quick!

Or WhatsApp us on +91 88501 69753

Chat Soon!