Inflation, Core Inflation, Food Inflation... You hear all these numbers

But why do they matter?

How do RBI and the Fed look at them?

How do these impact interest rate policy? And do interest rates matter to markets?

A quick look:

- The Fed and many other Central banks often talk of core inflation which is inflation net of food & fuel costs.

The logic being that this part cannot be targeted via interest rate actions of Central banks. Food inflation is often due to supply issues and interest rates which try to target demand in the economy may not be able to change food demand or prices.

- On the other hand, the RBI usually looks at total inflation. This time the Economic Survey said that RBI should start looking at inflation net of food.

- However this does not make so much sense for India because India is a much poorer country than the West.

Our per capita income is 3% that of the US (Yup, that's right) Even in PPP (purchasing power parity) terms, the US per capita income is about 10 times that for India.

- Hence food is a much larger component of the consumption basket for Indian - about 40-50% on the average, depending on which particular segment you take.

- Also, food inflation has been particularly high in the last few years.

As Sayantan Bera wrote in Mint quoting a RBI paper, food inflation averaged 6.3% during June 2020 to June 2024 compared to just 2.9% between 2016 and 2020.

- RBI cannot ignore food inflation in policy making because

1. Since food is such a big part of the household budget, if food inflation is high it reduces money available for other purchases.

If tuar daal prices go up, Indian households may cut back on toothpaste or soap - that's how precarious the situation is for them.

2. Food inflation results inflation elsewhere too - everything from transport prices to electrician charges go up and that is how food inflation leaks into the prices of other products.

3. One of the main areas targeted by central banks through interest rates is inflation expectations in the economy because that, in turn, drives actual inflation with a lag. If you expect inflation to be high you will ask for a higher salary raise, for example.

Since the individual does not make any distinction between inflation that comes via food or petrol prices versus inflation elsewhere, if food inflation remains persistently high it ups the inflation expectations in the country.

In my opinion, in a country like India, RBI has to take total inflation into account and not just inflation, net of food and fuel.

Why does the RBI's thinking matter to you?

Because interest rates have an impact on markets too. How? Had done a whole video on how that linkage works. Here's the link:

From the desk of

Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

...

- Share Via :

Data that I've highlighted multiple times in various articles and interviews over the last several months. Worth a recap:

1. The Smallcap index fell nearly 80% in 2008-9, it fell nearly two-thirds in 2018/19

When something falls 2/3rds, it can triple and you will make zero Returns.

The 2/3 years' returns of various small and micro cap managers or Smallcap funds being highlighted are to be seen in this context.

2. Another way of looking at it is that if something falls 80% and then compounds 50% for the next THREE years, you are still down about 1/3rd on your initial investment.

3. While in theory the 2008 high was breached in 2016, it was not the same index or stocks.

Many small caps that fall fade into oblivion. They NEVER come back.

The index churns 18-20% every year. In 5 years it's a new index altogether.

For context, about 4000 odd companies trade on the Indian stock exchanges today. The number of total listings till now is many times this number. There have been years with over a thousand IPOs.

4. While putting stop losses limit losses in large caps, they don't really work in small caps - where there is often no way to sell when everyone crowds the exits.

It is usually circuit down every day when these stocks fall!

5. Even hedging does not work for small caps as the only liquid puts available are for the Nifty - the small cap stocks do not move along with the Nifty.

Just to let you in on our strategy at First Global, we normally have 14-15% of our PMS portfolios in stocks between 1000 and 5000 crores market cap. We are currently around 7% in these. Yes, we are well aware that it may hurt relative performance in the short run but our first priority is to manage risk.

6. Can you choose wisely so that you're not caught in this trap when the bubble bursts?

Near impossible.

How many smallcaps did not fall in 2008/9? A grand total of 1%!

In 2018/19, the number was 8%

Do not fool yourself that your portfolio would consist of only these.

In this context, an old favourite from John Kenneth Galbraith's 'A Short History of Financial Euphoria'.

"There can be few fields of human endeavour in which history counts for so little as in the world of finance".

Time to get into a steadier stock portfolio.

Just to recap from our earlier statements, we do not expect a sustained crash in the large cap space invested in our PMS portfolios, although we are partially hedged. However smallcaps, microcaps, IPOs etc are areas where you should be super careful.

From the desk of

Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

...

- Share Via :

If you're on social media, you can't help but see the ads by various 'trainers' and finfluencers promising to teach you the mantras of successful stock/option trading.

A recent one promised a 'modest' return of 1% every trading day. With leverage and all, it's easy enough to demonstrate on an Excel sheet as something that is very doable.

But let us use the same Excel sheet to see what a 1% return on every trading day translates into.

With this return, and assuming 200 trading days, your money becomes over 7 times in ONE year.

So if you start with 10 lacs, you will end up with 70 lacs at the end of the first year. 4.9 crores at the end of 2 years. And it gets better!

You will nearly have nearly 1700 crores in 5 years and in 8 years' time you will be the richest Indian by a wide margin.

Now think.

If anyone has this magic formula why are they hawking it around for 5000 and 20000 Rupees? You have your answer.

Plus, as SEBI has been telling you, 90% of option traders LOSE money and even the balance 10% make only about 5000 rupees a month.

This is the data...the rest are fairly tales.

As an aside the chanting and dancing in some of these 'training programs' make them look like more cult than course.

From Your Friends at First Global

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

...

- Share Via :

The most deadly weapon in the financial world is the Excel spreadsheet.

Makes it seductively easy to make any kind of (fantasy) projections and sell stories based on that.

Some of them go right into lala land 🙃

Example: This company will grow earnings at 20% per annum for the next 25 years.

If you actually crunch the numbers, you will see that this means the profit will be up a hundred times.

Of course, you don't stop there. You now key in a fancy PE multiple on that profit and voila you can come up with any number you want for the projected share price.

No basic checks exist for these 'estimates'

-

What percentage will it be of the entire industry if its revenues grow at that rate?

-

What percentage will the revenues be of the GDP? Or the company's market capitalisation as a proportion of the total market cap of the country?

-

Most important, has there been even ONE company in history which has compounded profits 20% every year for 25 years?

-

Let alone that, ask people making these estimates to name the companies which have shown even 1% Profit growth every year for the last 25 years?

Go on...I'm waiting 😊

You will realise that it is a grand total of ONE company which has achieved that. Among listed companies in India, HDFC Bank is the only one which had shown any profit growth every year for 25 years.

But hey dragging a formula cell in excel is damn easy.

Actual execution by the company is near impossible.

Of course when the results don't keep up with the fanciful estimates, a whole bunch of factors can be blamed!

As always, success is attributed to great skill and failure to bad luck.

Unfortunately, listeners are equally happy to lap up fairy tales and following the Pied Piper into oblivion...with noone looking at data at all!

From Your Friends at First Global

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

...

- Share Via :

Till the end of October 2023, i.e., for the first 10 months of the year, the US Aggregate Bond Index was down almost 2.8% for the year.

As of last Friday, i.e., 3rd November 2023, it was down just 0.5% year-to-date.

So, what happened in just 3 days?

After all, a 2.3% move in half a week is significant even for equity indexes, let alone a supposedly stable US bond index.

Before getting into the details, let me broadly explain what caused long-term bond yields to decline.

As you know, when bond yields (or interest rates) go down, bond prices go up. Therefore, the upswing in the bond index actually reflected the decline in yields, especially for the 10 and 30-year bonds.

And why did these yields go down?

Because a number of macroeconomic indicators on economic activity and the labor market showed signs of a slowdown.

This was considered good news, as the Federal Reserve had desired this outcome. So if the economy slows down, the Federal Reserve (the Fed) was unlikely to raise rates and might cut interest rates sooner than expected. That's how the markets' logic went.

However, macroeconomics is a reflexive science, where things move in endless feedback loops.

Actions undertaken by central banks affect what happens in the economy and the markets, which, in turn, influences what central banks like the Fed, do. And on and on it goes.

During last week's meeting, the Fed was considered less hawkish on raising rates than before.

But what it actually said was this: They may not need to raise rates much because the market was doing the job for them by raising long-term yields, and other financial market indicators also showed tightening.

However, this statement itself brought long-term yields crashing down, which may, in turn, cause the Fed to become more hawkish.

The rates coming down and bonds rallying were also accompanied by rallies in other asset classes. In the past week, ETFs tracking stocks, government bonds, and corporate credit recorded their biggest weekly cumulative gain since November 2022. Even Emerging Markets, which have been relative underperformers, rallied.

Recently, correlations across asset classes have been positive not only during sell-offs but also in rallies, limiting diversification benefits.

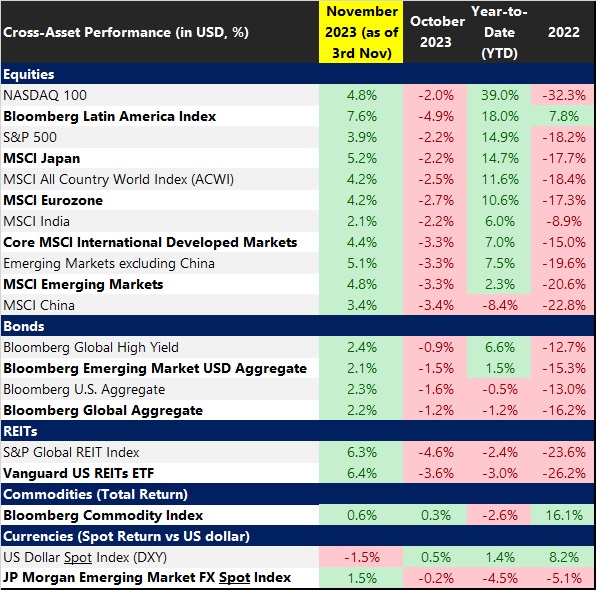

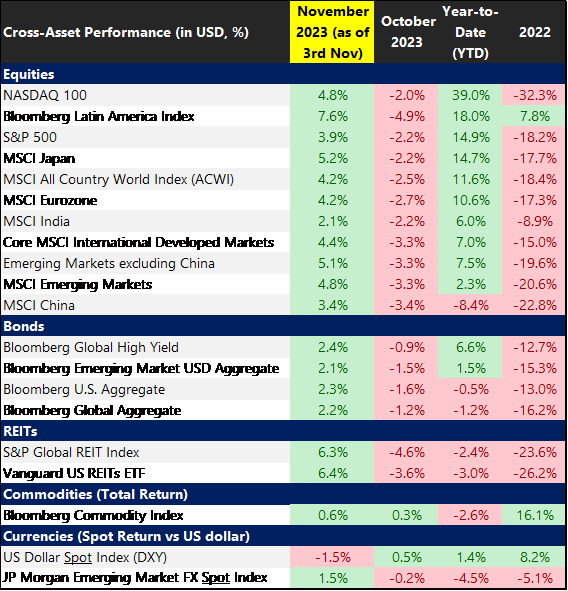

Here's a snapshot of the recent performance:

Source: Bloomberg, First Global

Data as of November 3, 2023

In the first three days of November 2023:

- Global equities, represented by the ACWI, saw an impressive gain of 4.2%. The Eurozone, EM ex-China, and Latin American markets posted gains of 4% to 7%. Notably, MSCI Japan recorded a robust 5.2% jump while MSCI South Korea soared 8.6%.

- In the bond market, high-yield bonds surged by 2.4%, while investment-grade bonds (IG) saw an increase of 2.2%. Real Estate Investment Trusts (REITs) experienced a strong 6.3% rebound from near 1-year lows.

- In the currency markets, the US dollar (DXY) depreciated by 1.5% to a 1-month low while the J.P. Morgan emerging market currency index strengthened by 1.5%.

What drove the rally?

Let’s dive into the sequence of events that led us to this wave of buying across assets:

- Monday, October 30: The US treasury department indicated that it would borrow $776 billion in the fourth quarter (Q4) of 2023 i.e. $76 billion less than it had anticipated in July.

For context, in the prior quarter i.e. Q3 2023, the treasury increased its net borrowing estimate to $1 trillion, well up from the $733 billion amount it had predicted in early May. The issuance jump for Q3 had pushed 10-year treasury yields higher by 100 basis points (bps) to 4.93% in 3-months.

While the drop in bond issuance from that high a level was taken as a positive sign, it still remains very elevated relative to history.

- Wednesday, November 1 (7 PM IST): Two days later, the US treasury department said that the issuance of longer-term securities, particularly 10-year notes, in Q4 of 2023 and Q1 of 2024 would not balloon as much as feared because it would shift issuance from longer-term securities to T-bills (1 month to 1 year) and to 2-year notes. Thus, long-term bond yields dropped, as markets expected a larger increase in supply, which could have pressured bond prices.

- Wednesday November 1 (7:30 PM IST): The US ISM Manufacturing PMI (Purchasing Managers Index), which is a monthly gauge of the level of economic activity in the manufacturing sector in the United States versus the previous month, contracted sharply in October, falling to 46.7, lower than the estimate of 49.0. This prompted a further drop in bond yields. Any reading below 50 indicates an anticipated contraction.

- Wednesday November 1 (11:30 PM IST): The U.S. Federal Reserve left interest rates unchanged. Fed Chair Powell's remarks appeared dovish relative to market expectations. His reference to higher longer-term rates as a reason to withhold further tightening created an awkward interdependency with the market.

Consequently, we witnessed a 10 bps drop in 2-year treasury yields to 4.84%, the lowest level since August 11 as the market moved to price in 100 bps of rate cuts by the end of 2024.

- Friday November 3: The highly anticipated US Non-Farm Payroll (NFP) report revealed that only 150,000 jobs were added in October (versus 180,000 expected). The September number was also revised lower to 297,000 from 336,000 earlier. Wages grew 0.2% month-on-month, below the expected 0.3%. The unemployment rate rose to 3.9% (vs 3.8% expected).

All these indicators showed that labor market was not as robust as earlier thought.

Since labor market tightness was one of the reasons for the Fed to raise interest rates, the cooling down reinforced expectations of a looser monetary policy, subsequently boosting prices in equities, bonds, and credit.

The all-important question: What's next?

The combination of the above-discussed data points has sparked hopes for a "Goldilocks" period -- a scenario where the possibility of ending rate hikes is considered in light of softer economic data, all while avoiding a full-fledged recession in the US economy.

Additionally, the size of the move in a fairly short period suggests a decent amount of short-covering as well.

Still, two key risks remain.

The Reflexivity Trap

Fed Chair Powell explicitly mentioned that he closely monitors multiple financial conditions indices. These indices take into account the movement in stocks prices, bonds yields, and credit spreads among others.

In his earlier press conferences, he stated that if the markets and financial conditions tighten, the Fed may need to raise rates by a much smaller amount because the macroeconomic consequences of tightening financial markets or the Fed increasing rates are the same.

If the current cross-asset rally continues, financial conditions could substantially loosen, potentially altering the Fed's policy stance and keeping rate hikes on the table.

Source: Bloomberg, First Global

Therefore, there is an implicit cap on the rally that can be expected from risky assets such as equities and corporate credit.

A greater than expected Economic Slowdown or Recession

Logically, the only way the Federal Reserve may refrain from considering any additional rate hikes or even potentially cut interest rates starting in the first half of 2024, is if the softer economic data does not stabilize and, in fact, deteriorates significantly.

But that will be bad news for corporate earnings and corporate credit.

Currently only scenario building and probabilities are possible. Making a firm prediction on how things pan out is not.

From Your Friends at First Global

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

...

- Share Via :

The Wait Is Finally Over: India Gets Included in JP Morgan’s Global Bond Index

JPMorgan announced on Friday, 22nd of September, that India's domestic bonds will be added to the Government Bond Index-Emerging Markets (GBI-EM), a global index tracked by approximately $236 billion in funds.

This inclusion is scheduled to commence on June 28, 2024, and will be phased in over a ten-month period, with incremental increases of 1% in its index weighting till India reaches the maximum allocation of 10%.

While the newspapers are full of how this marks the coming of age of the Indian bond market, let us examine the possible implications on a realistic and nuanced scale.

First the big picture:

- Yes, it should bring in some new funds into the Indian bond market. However, this will happen slowly. The inflows are anticipated at little above 21 billion US dollars over 10 months.

- If India is added on to other bond indices as well, this can help bring down interest rates a bit in India.

- The extra inflows are usually expected to help the local currency i.e. the Indian Rupee but given many other uncertainties in the Global macro economic environment, a strengthening is unlikely - though it may help stem the rupee depreciation slightly.

- Since most of the money is going into longer tenure securities, it may reduce the term premium (the higher yields for longer tenor bonds compare to short term interest rates) in the Indian bond market.

Now for the details

The Historical Context

India initiated discussions in 2019 regarding the incorporation of its debt into global indexes and explored clearing and settlement arrangements with Euroclear. In 2020, it removed foreign investment restrictions on certain government securities as part of its strategy to gain entry into global bond indexes. As a result, several bonds are now classified under the "Fully Accessible Route" with no foreign investment limitations. Part of the reason India has entered this index is also due to the gap created by the sanctions on Russia, which have taken away a significant market.

Concurrently, FTSE Russell, another index provider, is considering India's inclusion in its FTSE Emerging Markets Government Bond Index and will announce its decision on September 28.

What are the Implications?

At a time when global bond markets are experiencing uncertainty, the news of Indian government bonds being included in global bond indices is expected to have a stabilizing effect on Indian bond yields.

To put it simply, this means that the interest rates on Indian government bonds are likely to remain relatively steady. For instance, the benchmark 10-year Indian bond yields have ranged from 7.09% to 7.25% in September. In contrast, similar 10-year US bond yields increased by more than 40 basis points (bps) i.e. 0.4 percent point during the same period.

Looking ahead, if other index providers also add Indian bonds to their indices, it could lead to a longer-term positive effect, potentially resulting in lower interest rates in India.

This inclusion could also offer some relief for the Indian Rupee, which has been trading near its all-time low value. However, this doesn’t take away from the fact that ultimately the macro-economic environment reigns supreme.

With oil prices back above $90 a barrel, strong upside momentum in US treasury yields and the dollar, caution is warranted.

In our opinion, there's unlikely to be any significant fall in bond yields in the near term.

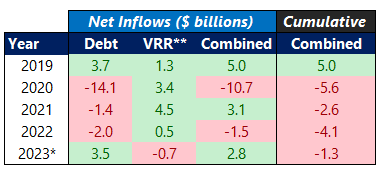

Expected Inflows into Indian Government Bonds Which Are Under-owned By Global Investors

Now, let's delve into the specifics. India is expected to have a maximum 10% representation in the GBI-EM Global Diversified Index. Currently, there are funds worth $213 billion that use this index as a benchmark. This means that we can anticipate an inflow of approximately $21.3 billion as a result of this inclusion, which will happen gradually. It begins with a 1% addition to the index on June 28, 2024, and will reach the maximum limit of 10% by March 31, 2025.

To put this expected influx of funds into perspective, consider the foreign portfolio investment (FPI) in Indian debt since 2019. After 2019, there were three years of continuous net outflows from debt investments. Even with the recent net inflow of nearly $3 billion year-to-date, we have not yet recovered from the substantial net outflow of $11 billion observed in 2020. Therefore, the anticipated inflow of over $20 billion resulting from the index inclusion could play an important role in financing the increased deficits and absorbing the increased supply of government bonds.

Debt Investments in India by FPIs

Data Source: NSDL

*As of September 22, 2023**

Investments via the Voluntary Retention Scheme

Characteristics of the Index Inclusion Securities

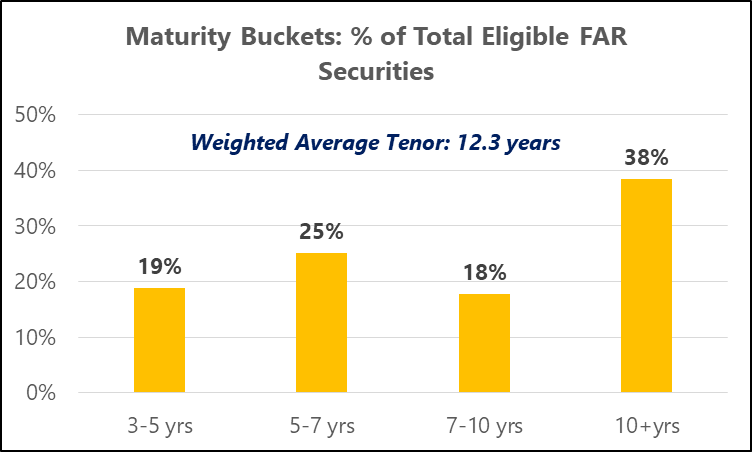

It's essential to note that only bonds issued under the government's Fully Accessible Route (FAR) are eligible for index inclusion. These FAR securities have no foreign portfolio investment limit.

To be eligible, these bonds must have a maturity of more than 2.5 years and a total outstanding size of at least $1 billion. This narrows down the selection to 23 out of the 31 bonds issued under the FAR route, with a combined outstanding value of $338 billion.

What's noteworthy is that the bid-offer spread (the difference between buying and selling prices) for FAR securities is more favorable compared to the current emerging market bonds in the index.

Additionally, FAR securities are significantly under owned by foreign portfolio investors, with only $9 billion invested in them compared to a total outstanding value of $338 billion. As a result, there is a significant potential for substantial foreign portfolio investment inflows into these securities.

The weighted average maturity of these eligible FAR securities is relatively long, at 12.3 years. Nearly 40% of the incoming funds are expected to flow into Indian government securities with maturities of 10 years or more. This could lead to a reduction in the term premium.

Term premium, in simple terms, represents the extra yield that longer-term bonds offer compared to shorter-term ones. Historically, this premium has averaged around 90 basis points (0.9%). In other words, 10-year bonds, on average, yield 0.9% more than 1-year bonds.

Source: CCIL, First Global

However, the term premium is influenced by economic cycles. During periods of interest rate cuts, short-term bond yields tend to fall more compared to longer-term yields, steepening the yield curve and increasing the term premium. Conversely, during rate hike cycles, as we are witnessing now, the term premium can decrease or even turn negative.

If the supply of government bonds with maturities of 10 years and above does not increase to match the expected demand from passive inflows, we could see a decline in the term premium as demand outpaces supply.

Looking Ahead

In the long term, the movement of Indian bond yields is expected to align more closely with the global economic environment. This is because active investors may also increase their participation in Indian bonds.

The volatility of flows may increase during times of global financial stress as assets under management of the emerging market bond funds fluctuate. Currently, foreign portfolio investors are utilizing only 23.8% of the allotted limits for investing in Central Government Securities.

Considering the current global scenario, including the price of Brent oil at $90 a barrel, the US dollar's strong performance with a 5.5% yield advantage, and Indian government bond yields hovering around 7% with real yields slightly lower than those of their US counterparts, it is unlikely that we will see a significant rally in Indian government bonds.

Therefore, it's advisable not to make investment decisions solely based on this news unless there are other relevant macroeconomic developments to consider.

From Your Friends at First Global

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

...

- Share Via :