The Wait Is Finally Over: India Gets Included in JP Morgan’s Global Bond Index

JPMorgan announced on Friday, 22nd of September, that India's domestic bonds will be added to the Government Bond Index-Emerging Markets (GBI-EM), a global index tracked by approximately $236 billion in funds.

This inclusion is scheduled to commence on June 28, 2024, and will be phased in over a ten-month period, with incremental increases of 1% in its index weighting till India reaches the maximum allocation of 10%.

While the newspapers are full of how this marks the coming of age of the Indian bond market, let us examine the possible implications on a realistic and nuanced scale.

First the big picture:

- Yes, it should bring in some new funds into the Indian bond market. However, this will happen slowly. The inflows are anticipated at little above 21 billion US dollars over 10 months.

- If India is added on to other bond indices as well, this can help bring down interest rates a bit in India.

- The extra inflows are usually expected to help the local currency i.e. the Indian Rupee but given many other uncertainties in the Global macro economic environment, a strengthening is unlikely - though it may help stem the rupee depreciation slightly.

- Since most of the money is going into longer tenure securities, it may reduce the term premium (the higher yields for longer tenor bonds compare to short term interest rates) in the Indian bond market.

Now for the details

The Historical Context

India initiated discussions in 2019 regarding the incorporation of its debt into global indexes and explored clearing and settlement arrangements with Euroclear. In 2020, it removed foreign investment restrictions on certain government securities as part of its strategy to gain entry into global bond indexes. As a result, several bonds are now classified under the "Fully Accessible Route" with no foreign investment limitations. Part of the reason India has entered this index is also due to the gap created by the sanctions on Russia, which have taken away a significant market.

Concurrently, FTSE Russell, another index provider, is considering India's inclusion in its FTSE Emerging Markets Government Bond Index and will announce its decision on September 28.

What are the Implications?

At a time when global bond markets are experiencing uncertainty, the news of Indian government bonds being included in global bond indices is expected to have a stabilizing effect on Indian bond yields.

To put it simply, this means that the interest rates on Indian government bonds are likely to remain relatively steady. For instance, the benchmark 10-year Indian bond yields have ranged from 7.09% to 7.25% in September. In contrast, similar 10-year US bond yields increased by more than 40 basis points (bps) i.e. 0.4 percent point during the same period.

Looking ahead, if other index providers also add Indian bonds to their indices, it could lead to a longer-term positive effect, potentially resulting in lower interest rates in India.

This inclusion could also offer some relief for the Indian Rupee, which has been trading near its all-time low value. However, this doesn’t take away from the fact that ultimately the macro-economic environment reigns supreme.

With oil prices back above $90 a barrel, strong upside momentum in US treasury yields and the dollar, caution is warranted.

In our opinion, there's unlikely to be any significant fall in bond yields in the near term.

Expected Inflows into Indian Government Bonds Which Are Under-owned By Global Investors

Now, let's delve into the specifics. India is expected to have a maximum 10% representation in the GBI-EM Global Diversified Index. Currently, there are funds worth $213 billion that use this index as a benchmark. This means that we can anticipate an inflow of approximately $21.3 billion as a result of this inclusion, which will happen gradually. It begins with a 1% addition to the index on June 28, 2024, and will reach the maximum limit of 10% by March 31, 2025.

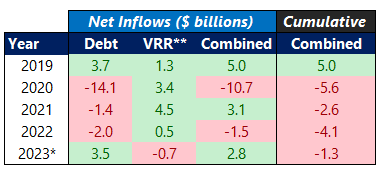

To put this expected influx of funds into perspective, consider the foreign portfolio investment (FPI) in Indian debt since 2019. After 2019, there were three years of continuous net outflows from debt investments. Even with the recent net inflow of nearly $3 billion year-to-date, we have not yet recovered from the substantial net outflow of $11 billion observed in 2020. Therefore, the anticipated inflow of over $20 billion resulting from the index inclusion could play an important role in financing the increased deficits and absorbing the increased supply of government bonds.

Debt Investments in India by FPIs

Data Source: NSDL

*As of September 22, 2023**

Investments via the Voluntary Retention Scheme

Characteristics of the Index Inclusion Securities

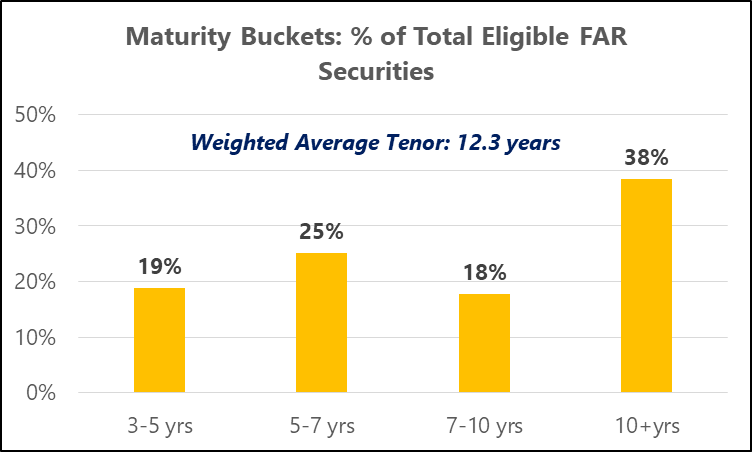

It's essential to note that only bonds issued under the government's Fully Accessible Route (FAR) are eligible for index inclusion. These FAR securities have no foreign portfolio investment limit.

To be eligible, these bonds must have a maturity of more than 2.5 years and a total outstanding size of at least $1 billion. This narrows down the selection to 23 out of the 31 bonds issued under the FAR route, with a combined outstanding value of $338 billion.

What's noteworthy is that the bid-offer spread (the difference between buying and selling prices) for FAR securities is more favorable compared to the current emerging market bonds in the index.

Additionally, FAR securities are significantly under owned by foreign portfolio investors, with only $9 billion invested in them compared to a total outstanding value of $338 billion. As a result, there is a significant potential for substantial foreign portfolio investment inflows into these securities.

The weighted average maturity of these eligible FAR securities is relatively long, at 12.3 years. Nearly 40% of the incoming funds are expected to flow into Indian government securities with maturities of 10 years or more. This could lead to a reduction in the term premium.

Term premium, in simple terms, represents the extra yield that longer-term bonds offer compared to shorter-term ones. Historically, this premium has averaged around 90 basis points (0.9%). In other words, 10-year bonds, on average, yield 0.9% more than 1-year bonds.

Source: CCIL, First Global

However, the term premium is influenced by economic cycles. During periods of interest rate cuts, short-term bond yields tend to fall more compared to longer-term yields, steepening the yield curve and increasing the term premium. Conversely, during rate hike cycles, as we are witnessing now, the term premium can decrease or even turn negative.

If the supply of government bonds with maturities of 10 years and above does not increase to match the expected demand from passive inflows, we could see a decline in the term premium as demand outpaces supply.

Looking Ahead

In the long term, the movement of Indian bond yields is expected to align more closely with the global economic environment. This is because active investors may also increase their participation in Indian bonds.

The volatility of flows may increase during times of global financial stress as assets under management of the emerging market bond funds fluctuate. Currently, foreign portfolio investors are utilizing only 23.8% of the allotted limits for investing in Central Government Securities.

Considering the current global scenario, including the price of Brent oil at $90 a barrel, the US dollar's strong performance with a 5.5% yield advantage, and Indian government bond yields hovering around 7% with real yields slightly lower than those of their US counterparts, it is unlikely that we will see a significant rally in Indian government bonds.

Therefore, it's advisable not to make investment decisions solely based on this news unless there are other relevant macroeconomic developments to consider.

From Your Friends at First Global

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!