We all know that the Reserve Bank of India (RBI) kept its repo and reverse repo rate — which are at a record low level — unchanged at 4% and 3.35%, respectively, while forecasting inflation to subside to 4.2% by Q4 in 2022-23 from 5.6% currently.

This inflation rate being forecast is for the Consumer Price Index (CPI). The inflation forecast came in below consensus, surprising the markets.

In contrast, the wholesale inflation (based on the Wholesale Price Index) has been much higher. So, we have a situation where producers are facing the highest inflation in two decades, which is not reflecting in consumer prices and that has implications for us not just as consumers but also investors.

In normal times, the CPI follows the WPI with a lag, as input price hikes are passed on to consumers over time. This time, the divergence has persisted for several quarters.

Shorn of macroeconomic jargon, this means that companies are facing cost increases that they are unable to pass on to end consumers, probably because consumer demand is not so buoyant.

This translates into margin pressures that are already visible across the board in Q3 FY22, in diverse industries from FMCG to autos to chemicals to capital goods. This trend will only accelerate in the current quarter and beyond.

For the market as a whole, operating profit margins for a sample of 432 companies (excluding banks and financials) contracted 200 basis points year-on-year (Y-o-Y) as raw materials costs jumped 466 basis points Y-o-Y.

Now for the details:

India’s WPI is at a Record 13.6%, the Highest in Two Decades

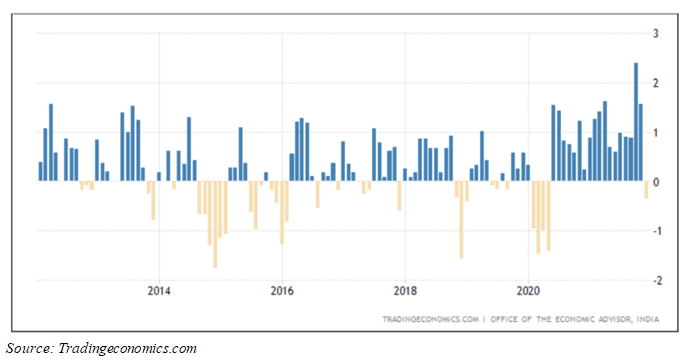

The WPI stood at a two-decade high of 13.6% year-on-year (Y-o-Y) in December 2021, albeit down marginally from a peak of 14.2% in November, as inflation quickened for primary articles (13.4% versus 10.3%), with prices of food articles jumping sharply (9.6% vs 3.7%). Although base effects can play a role in Y-o-Y numbers, month-on-month numbers also remain strong, as is evident from the chart below.

India's wholesale price inflation consistently above 1-1.5% M/M (month over previous month) since H2 CY 2020.

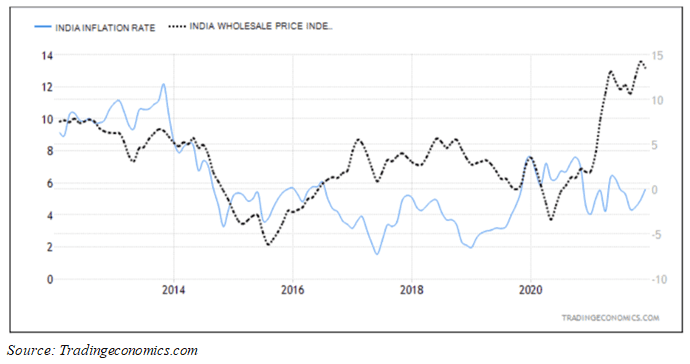

So, this should show up in the consumer price inflation, right? Well, the headline CPI is still under the RBI’s target band i.e. 4% +/- 2 percentage points. India's retail price inflation rose to 5.6% in December 2021 from 4.9% in the previous month. Although one would expect CPI to lag WPI by some period of time, the two data points have been diverging quite dramatically this time around.

The rising divergence between India’s WPI (right, % Y-o-Y) and CPI (left, % Y-o-Y)

And the result is predictable:

Companies face unprecedented margin pressure as input cost inflation surges

The way we interpret the divergence between Wholesale Price Inflation and Consumer Price Inflation is this: the majority of the companies that are facing rising input costs have been unable to completely pass on these price increases to the consumers. They are taking a significant hit on their margins to remain competitive and protect sales in an uncertain environment — at least that’s what the corporate results and forward guidance is telling us.

Operating profit margins for a sample of 432 companies (excluding banks and financials) contracted 200 basis points year-on-year (Y-o-Y) as raw materials costs jumped 466 basis points Y-o-Y. High costs ate into margins.

For example, BHEL’s gross margins were down 100 bps Y-o-Y, hit by higher commodity prices on nearly 50% of fixed price-based order backlog. Marico’s consolidated gross margins fell 320 bps. JSW Steel’s EBITDA margin contracted nearly 500 bps Y-o-Y, though net sales were up 50% Y-o-Y. Bajaj Auto’s EBITDA margin, for instance, contracted 420 basis points Y-o-Y, driving down the EBITDA by 21% Y-o-Y. At Havells’ gross margins crashed 583 bps, driving down EBITDA margins by nearly 400 bps, despite revenues rising by 15.4% Y-o-Y. Also, the EBIDTA margin of Asian Paints was down 8.2 percentage points Y-o-Y, though revenues were up 25.6% Y-o-Y, while the EBIDTA margin of BASF Ltd was down 4.1 percentage points Y-o-Y, in spite of revenues being up 36% Y-o-Y. Pidilite also faced continued pressure on prices due to high input costs and in spite of its revenues being up 24% Y-o-Y, EBIDTA margins were down 861 basis points Y-o-Y and even down 167 basis points Q-o-Q. Also, Deepak Nitrite’s EBIDTA margin at 20.4% in Q3FY22 was down 671 basis points, in spite of top line being up 39.5% Y-o-Y. These examples are only illustrative of margin pressures across a variety of industries.

Thus, RBI’s over-optimism on the inflation front overlooks the issues being faced by Indian companies. Investors need to be cautious on their sector plays and not get carried away by under-control CPI print (for now) and a dovish RBI policy.

As to why the producers are facing high inflation, the answer mainly lies in commodity prices, although supply bottlenecks and high international shipping costs, among others, have all contributed.

A big driver of wholesale price inflation is the rise in commodity prices

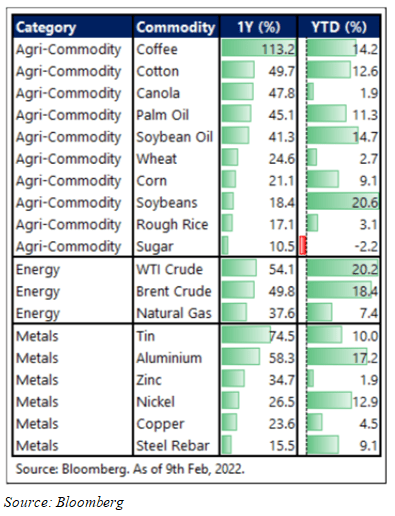

Whether you look at year-on-year or year-to-date numbers, commodity price inflation seems rampant across the board from agricultural commodities such as coffee (+113% Y-o-Y) to crude oil (+54% Y-o-Y) to aluminium (+58% Y-o-Y). Apart from severe undersupply, as indicated by bumper premiums being paid for immediate supply (known as backwardation in market parlance), structural forces such as the accelerated transition to green energy have also been contributing to high fossil fuel prices (owing to underinvestment and supply constraints). This phenomenon is also sometimes referred to as “Greenflation”. Meanwhile, exorbitantly high natural gas prices across Europe have led to sizeable cuts in smelter production wreaking havoc on metal supplies and inventories, thus pushing prices higher in a reflexive loop.

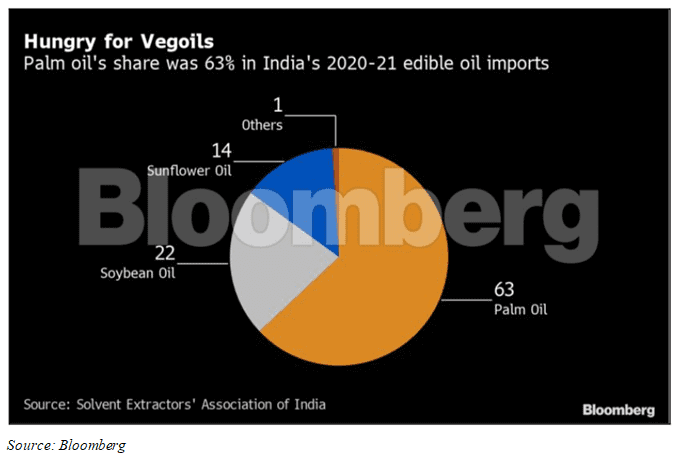

According to the Food and Agriculture Organization (FAO), world food prices rebounded in January and remained near 10-year highs, led by a jump in the vegetable oils index (+4.2% month-on-month). Prices of palm oil, the most-consumed edible oil in the world, have jumped 12% this year to a record, while rival soybean oil has gained 15%, putting a strain on India, the top buyer of soybean and sunflower oils.

Higher oil prices also result in price hikes in a variety of downstream and derived chemicals.

Overall, the manufacturers are caught in a bind with higher costs and a relatively sluggish demand making price hikes in finished goods difficult. A situation worth watching.

(A version of this article first appeared in The Economic Times)

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side, super quick!

Or WhatsApp us on +91 88501 69753

Chat Soon!