2022 has not been particularly great for equity portfolio management from the word go and most major markets have been in the red zone. The Russia-Ukraine conflict has only made it clearer that there are few places to hide in the current environment.

But a more careful look shows that there is a category of countries/markets that have actually done well in spite or sometimes because of the current turmoil.

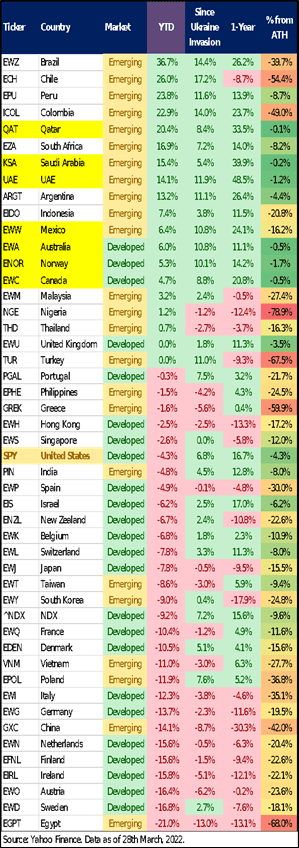

A quick country performance snapshot shows that Australia, Saudi, Canada, Qatar, UAE, and Norway are hitting all-time highs (ATH) or are within 1-2% of the same. There are some others (especially those from South America like Brazil, Chile etc) which may be still away from their All-time highs but have done very well of late.

The common theme is that most of the global investing markets doing well are those of resource-rich countries benefiting from the current commodity rally.

Out of the top 20 performers year-to-date (YTD) meaning since January 1, 2022, 15 or 75% are emerging markets (EMs) with Latin America leading the race – Brazil (+37%), Chile (+26%), Peru (+24%), and Colombia (+23%). Most have natural resources heavy GDP/ export composition. For instance, Brazil is a large exporter of iron ore, soyabean & a host of other agricultural products as well as crude oil/ downstream products. Nearly half of Peru's exports relate to copper and gold. And so on.

The only developed markets (DMs) making it to the top 20 are Australia (+6%), Norway (+5.3%), Canada (+4.7%), the UK (+0%), and Portugal (-0.3%) - most of which are large exporters of commodities. Canada and Norway for example, are significant players in the energy market, Australia in the ores market.

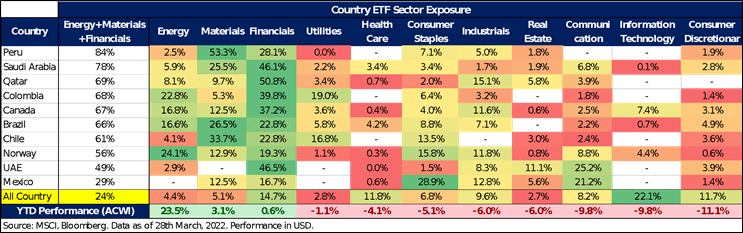

Although idiosyncratic factors such as political risk premiums along with valuations might play a role, a look at the sector composition reveals that the exposure to top-performing sectors i.e. Energy, Materials and Financials is particularly high in these high-performing countries (50-80%) compared to just 24% for the All Country World Index (ACWI) - a global equity index.

Why does this sector composition matter? Because Energy, Materials and Financials are the only sectors that have given a positive return this year so far.

Not surprising, given that commodity prices have rallied sharply in the past few months. This has meant an advantage for resource-rich countries rather than those that rely more on the manufacturing sector.

Prices for oil, gas, metals, agricultural products etc. have all been zooming. This is good news for the miners/ producers of these products and bad for the users of these products like those making consumer staples.

For example, if the prices of metals go up, it increases the cost of manufacturing a car. Similarly the increase in prices of agriculture oils as well as downstream petrochemical products mean higher costs for those making consumer staples, from shampoos to food.

On the flip side, the broad global equity index ACWI has the highest allocation to the worst-performing sectors such as Information Technology (-9.8% YTD) and Consumer Discretionary (-11.1% YTD) at a combined 34% while exposure of the top performing countries to these sectors is just 4% on average, thus explaining a large chunk of their outperformance.

In a nutshell, the top performing countries tend to be resource-rich which shows in the high weightage to Energy and Materials (plus Financials) and have low exposure to technology and consumer products, the currently laggard industries.

Elsewhere, South Africa, a well-known commodity producer, especially for precious metals, is also up 17% YTD while in Asia, despite the carnage in Chinese equities (-14%), Indonesia, again a natural resource/ agricultural commodities rich country, remains the top performer YTD with a 7.4% gain, followed by Malaysia (+3.2%) and Thailand (+0.7%).

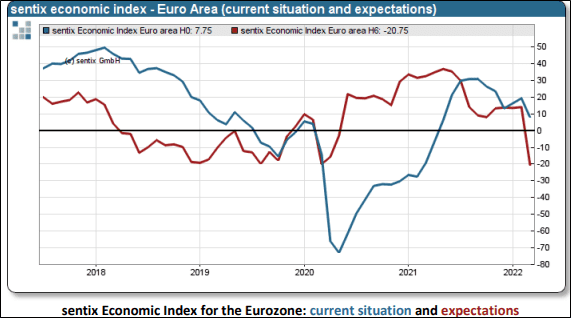

At the bottom of the barrel is Europe with Austria, Sweden, Netherlands, Germany all down 14-17% YTD with 20%+ drawdowns, as the region deals with burgeoning energy and food costs on the back of the ongoing Russia-Ukraine war. Recent data showed that the Eurozone economic expectations index plunged by -34.75 points, the largest drop in the 20-year history of the sentix economic index.

For now, the global investing markets are reflecting the fact that commodity prices are and continue to be on the way up. So, depending on whether that constitutes the output or the input for an industry/ sector, it gets reflected in its market performance.

Broadly speaking if you are a commodity producer your margins and profits will go up whereas if you are a commodity user your margins and profits will go down. In India also, that is a good framework to use when analyzing sectors and companies.

This same phenomenon is reflected at the country level with commodity rich countries seeing a run up in the stock markets even as there is weakness almost everywhere else.

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!