After decades of being confined to history books at least for the Western world, inflation has been making a comeback for the last few quarters.

It started with the rally in commodities, especially oil and metals, post Covid in 2020 after a 10-15 year period when various commodity prices had remained largely subdued.

After some ups and downs in 2021, the prices started to accelerate around the beginning of the New Year. Added to this cyclical upturn have been climate events impacting agriculture produce; supply disruptions thanks to the pandemic and so on - all of which have contributed to an upward pressure on prices.

In the US and some other developed economies, housing prices have also been on a run as many government policies to help the citizens over the hump of the pandemic resulted in excess liquidity for households, especially as spending options were limited thanks to the pandemic. This liquidity was partly used for real estate purchases. Therefore, many components of the consumption/ inflation basket had been seeing rising prices over the second half of 2021.

Several central banks assessed that the supply constraint causing part of this inflation would ease over time and the inflation would prove to be transitory. This proved to be more of a hope than anything else, with inflation continuing to persist.

These trends accelerated with the rising Russia Ukraine tensions early in this year culminating in a full-fledged war by the end of February. Even before the actual war on the ground, prices of a whole lot of commodities from crude oil and natural gas to aluminum, palladium, nickel, potash to wheat & edible oils had already risen 20 to 30% since January 1.

This has only accelerated since the actual conflict began. Plus, there have been fresh disruptions to shipping and supply chains as well as to agriculture production cycles in Ukraine and to some extent Russia, which will result in production shortfalls.

Let us look at how this has impacted various nations of late as per the inflation figures which have been released for several major economies over the past few days.

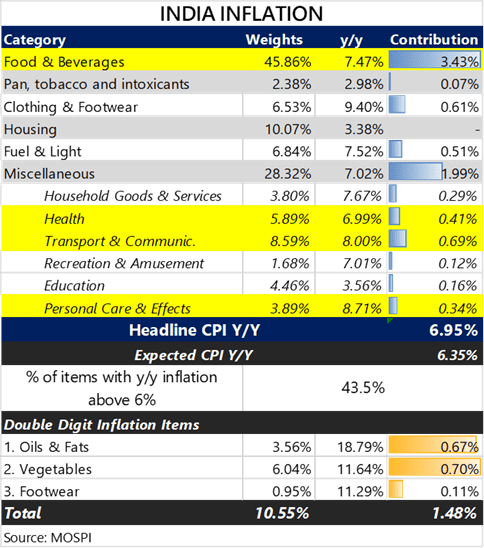

INDIA: Inflation Leaks Beyond the Commodity Categories...Likely to Impact Demand

India's headline CPI hit 6.95% in March 2021 year on year (y/y), meaning over the same period last year. It is also up 0.96% month on month (m/m), i.e. over February 2022. This is the highest since November 2020.

Food & Beverages which account for almost half of the index jumped 7.5% y/y, thus contributing to more than 60% of the y/y acceleration in prices, led by double-digit increases in Oil & Fats (18.8% y/y) and Vegetables (11.6% y/y) which together account for about 9.4% of the index.

This isn't surprising given that the UN FAO’s global Food Price Index surged 13% m/m in March to a record high amidst constrained supplies (Russia-Ukraine war) and adverse weather conditions. As edible oil prices have risen 50-70% above pre-Covid levels, 24% of Indian households have cut down consumption while 67% are paying more for it by reducing spending and savings, shows a survey by LocalCircles.

However, clearly inflation has spread beyond the more directly explainable categories like edible oils. For example, the prices in the clothing and footwear category are up 9% year on year and even several services like health, transportation & communication, recreation etc. have seen 7-8% y/y inflation. All of this shows that inflation is becoming more entrenched.

This is in spite of the fact that the high Wholesale Price Index (WPI) inflation which has remained or about 13-14% for several months now has not really translated to that extent into higher consumer price inflation, as producers are still trying to hold back price increases given sluggish demand. However, given the recent runaway increase in commodity prices, they don't have much of a choice and consumer prices are beginning to rise for manufactured products as well.

As consumers have to pay more both for food as well as other daily use items, the discretionary spend is and will continue to get postponed.

The impact of fuel prices also is not visible in these numbers as those hikes have happened more recently. Fuel prices not only have a direct impact on the household budget but over time show up in higher prices of most goods and services as those have a transport component. This impact will be visible April onwards.

In our view, inflation is expected to accelerate in India over the next few months before it starts to moderate once the base effect kicks in (when the comparable period becomes a period of high inflation in the previous year). This will also impact the demand for a variety of goods, besides putting upward pressure on interest rates (already visible) and downward pressure on the Indian Rupee.

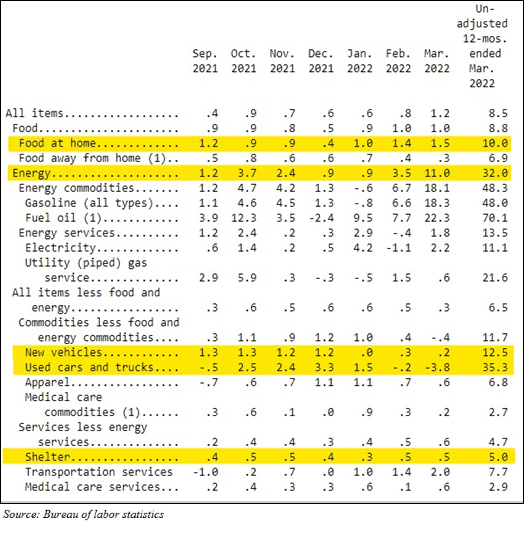

UNITED STATES: Non food and Fuel Inflation Begins to Moderate

US CPI y/y Actual 8.5% (Forecast 8.4%, Previous 7.9%)

US Core CPI (excluding food and fuel) y/y Actual 6.5% (Forecast 6.6%, Previous 6.4%)

US CPI m/m Actual 1.2% (Forecast 1.2%, Previous 0.8%)

US Core CPI m/m Actual 0.3% (Forecast 0.5%, Previous 0.5%)

Reaction: US treasury bonds rallied 6-10 bps as the curve bull steepened on softer than expected core CPI; the US dollar index (DXY) which measures the US Dollar against a basket of other currencies sold-off initially but settled 0.3% higher at 100.3, close to a 2-year high.

While headline inflation remained high, core Inflation, which excluded food and fuel, came in below consensus as Food at Home (1.5% m/m) and Energy (+11% m/m) were the main culprits.

Used Car & Trucks whose prices went through the roof in 2021 due to supply constraints for new vehicles, showed a decline in prices of 3.8% m/m which is a good sign.

However, the contribution of shelter inflation which measures housing costs, will remain sticky (+0.5% m/m, 5% y/y) due to lagged effects of soaring rents (refer to this paper for more details) and high weightage (33%) even as mortgage rates jump to 5.1%.

Overall, inflation may remain sticky at levels much higher than 2% (which has important ramifications on the monetary policy of the Fed and its rate hikes), there are signs that we are at or close to peak inflation in the US, given that price gains in food & energy as witnessed in the last 1-2 years are hardly sustainable without demand destruction and that base effects might also come in to play soon enough.

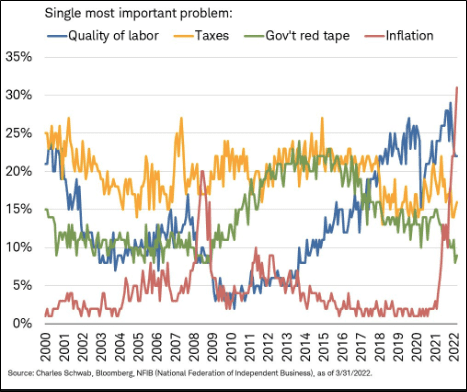

Elsewhere, according to the NFIB Small Business Survey released today, 31% of business owners identified inflation as their single most important problem, the biggest share since the Q1 of 1981, replacing worries about "labor quality" as the No.1 problem. The survey may be hinting at broader issues regarding the inflation pass-through capacity, given that inflation may not be a problem for businesses if growth/demand is also strong.

UNITED KINGDOM: Inflation Expectations Remain Worryingly High

UK CPI y/y Actual 7% (Forecast 6.7%, Previous 6.2%) -- 30-year high

UK CPI m/m Actual 1.1% (Forecast 0.8%, Previous 0.8%)

UK Core CPI, net of food and fuel, y/y Actual 5.7% (Forecast 5.3%, Previous 5.2%)

UK Core CPI, net of food and fuel, m/m Actual 0.9% (Forecast -, Previous 0.8%)

The headline and core CPI continue to be higher than expected with the Citi UK Inflation Surprise Index also hovering around its all-time-highs. Motor fuels prices surged 9.9% from February, the biggest increase in 31 years.

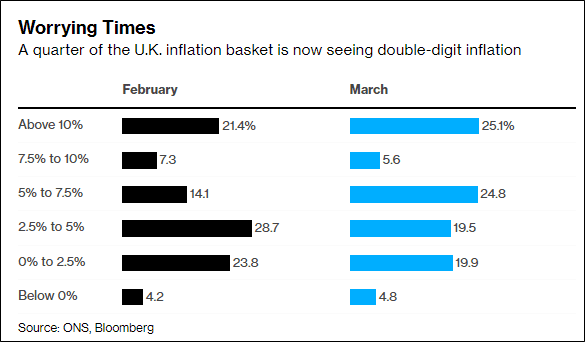

Market implied rates (meaning inflation expectations) such as those indicated by inflation swaps in the UK are priced for 9.6% inflation over the next 1 year (Note: In April, a 54% increase in energy bills is set to kick in, adding about 1.8 points to the headline rate) and gradually moving lower to average 5% average over the next 5 years. Longer term inflation expectations as indicated by 5-year forward 5-year inflation rate have been trending higher for more than year and currently sit at ~4% i.e. double the Bank of England’s target of 2%. The breadth and severity of the inflation has accelerated to worrying levels indeed (see image below). Large retailers such as Tesco have already issued profit warnings on the back of this.

The table above gives the percentage of items from the inflation calculation categories that fall in each inflation band. Thus 25% of the categories for which prices are measured, saw a 10% plus increase in inflation.

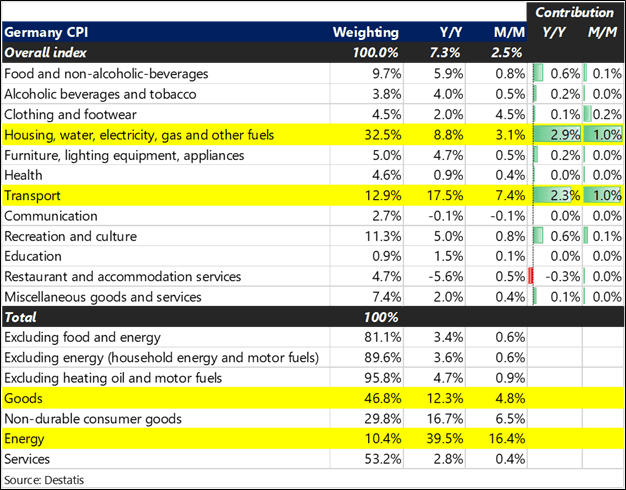

GERMANY: Headed into Historically High Inflation

German headline CPI comes in at 7.3% y/y the highest since 1981 while the m/m print of 2.5% is the largest since October 1952 - led primarily by food and energy (ex-food/energy is 0.6% m/m and 3.4% y/y). Goods inflation continues to dominate at 4.8% m/m and 12.3% y/y vs. 0.4% m/m and 2.8% y/y for services. Meanwhile, WPI registers another record peak of 22.6% y/y and 6.9% m/m.

Germany has traditionally been an inflation hawk due to the country's bout with hyperinflation almost 100 years back.

However this time it held back on raising interest rates for a long time but obviously such historic levels of inflation have now put pressure on Bond yields in the EU as well.

Here's how 10 year Treasury bond yields have moved across the EU from January 1 till date (bps stands for basis points 100 basis points = 1 percent points)

Germany: +90bps to 0.79%

France: +107bps to 1.27%

Spain: +110bps to 1.72%

Italy: +120bps to 2.39%

UK: +83bps to 1.82%

Poland: +240bps to 5.90%

Hungary: +227bps to 6.67%

Czech Republic: +110bps to 4.10%

Across the world, inflation will continue to be the most watched macro variable this year that will, in turn, be the key factor driving interest rate moves by Central Banks from the RBI to the Fed. The rate changes in turn are big determinants of valuations in both equity and fixed income markets. This will be the space to watch.

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!