While economists and analysts have been calling for peak inflation for almost a year now, prices have kept going up rapidly, thanks to China’s zero-COVID policy, the Russia-Ukraine war, and chronic underinvestment in fossil fuels, being combined with re-opening in most countries.

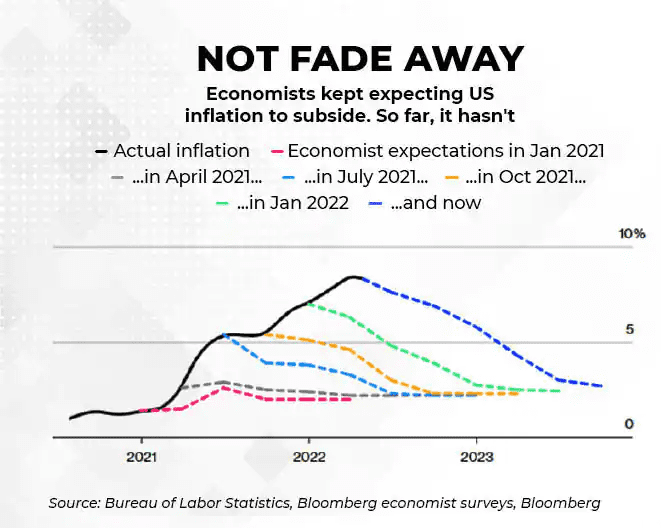

As the Dutch proverb goes, “It is hard to make predictions, especially about the future!” Economists’ forecasts of inflation over the last few quarters bring this adage to mind.

Given below is the actual and forecast US inflation graph from January 2021 onwards ― the dotted lines are the predictions. Till the actual Consumer Price Index (CPI) inflation was below the 2 percent number targeted (1.4 percent in January 2021 and 1.7 percent in February 2021), the economists could envisage a slight increase before it obediently fell back. Thereafter, they could only see it trend down because it was unthinkable (to them) that inflation could actually be higher than 2 percent on sustained basis.

For an entire generation which had grown up with inflation being only a theoretically targeted variable for the Western Central banks, it was unimaginable that it would actually become something that was front and centre and to be managed.

Never mind that the amount of money being pumped into the system by the Fed and some of the other Central banks was also unprecedented by an order of magnitude, or that supply chain disruptions were also on a scale not seen in a globalised world for decades.

The economists simply could not visualise a reality where inflation sustained above 2 percent. Therefore, once it did exceed 2 percent, every month the economists predicted that the inflation for that month would be the peak inflation and would go down thereafter.

Except that the inflation numbers refused to keep to this diktat and continued to climb.

While economists and analysts have been calling for peak inflation for almost a year now, prices have kept going up rapidly, thanks to China’s zero-COVID policy, the Russia-Ukraine war, and chronic underinvestment in fossil fuels, being combined with re-opening in most countries.

In a piece I wrote last month on global inflation, I had expressed hope that we may be nearing peak inflation in the US but this was probably not the case either in Europe or in India. So, how have things panned out since?

The peak inflation in the US has got pushed forward a bit, mainly because the shelter inflation which captured housing-related costs has not gone down as anticipated. This is because US residents are scrambling to buy houses and lock in mortgage rates which are anticipated to rise further as the Fed tightens. The size of the mortgage market is still running far ahead of ‘normal’ levels. We expect this to cool off in the next month or two and hence, be past peak inflation in the US.

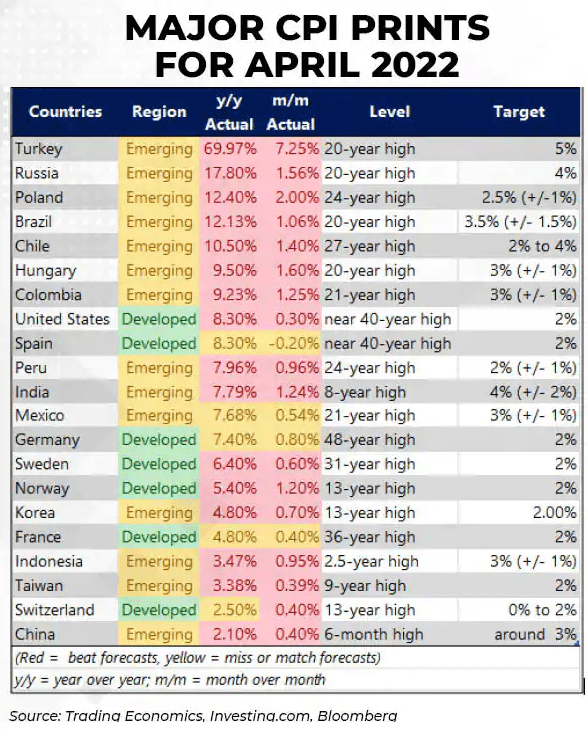

Now, as to why the economists got it so wrong is because inflation, if not at unprecedented levels, is definitely at several decades’ high for many countries around the world, especially in the developed world. It would have just appeared safer to stick to the old script than to make a call that something unprecedented was happening.

To put this in context, in the US and Spain, inflation is touching 40-year highs, in Germany nearly a five-decade high. Across countries, two-three-decade highs are common.

In India while the CPI is beyond the Reserve Bank of India’s (RBI) tolerance levels, the eye-popping number is the Wholesale Price Index (WPI) where inflation has exceeded 15 percent for the month and breached a three decade high for the annual number.

CPI data for April shows that both month-on-month (MoM), ie April 2022 over March 2022, and year-over-year (YoY), ie April 2022 over April 2021, inflation have come in above estimates and remain two to four times higher than the respective targets in most countries.

Asia, which had been lagging other Emerging Markets (EMs) lately, has caught up with price increases in Korea, Taiwan, and India hitting eight-13 year highs. As a result, we witnessed an interim rate hike of 40 basis points (bps), i.e. 0.4 percentage points, by the RBI while the Bank of Korea (BoK) Governor Rhee Chang-yong said he could consider bigger interest rate increases (vs 25 bps standard), depending on data that will become available around July and August.

Now for what's happening country/region-wise, especially in India and the US.

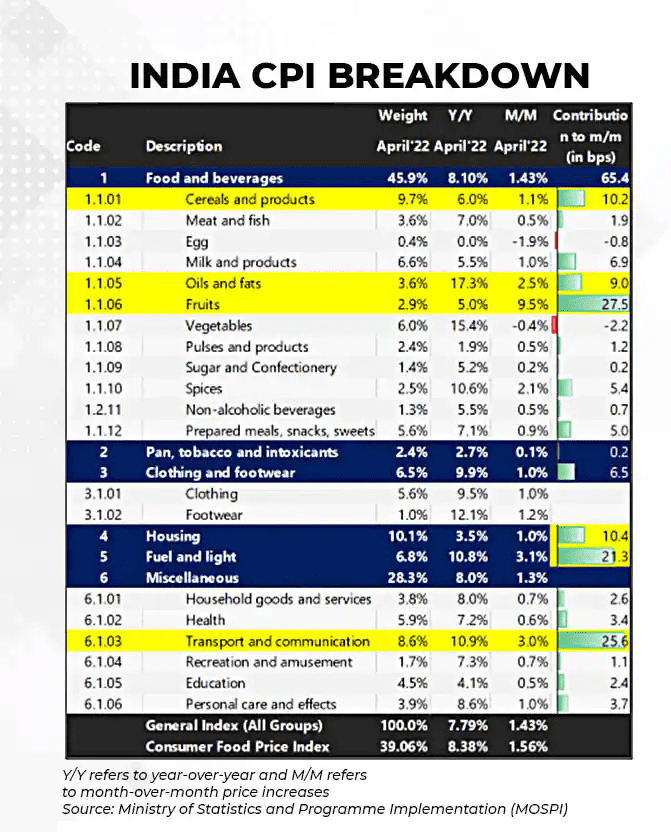

India CPI hits 8-year high...but wholesale inflation remains way higher

Up until now the impact of WPI inflation in India was not fully evident in the CPI even beyond the expected lag.

Unlike in the US, the Indian consumer and her household budget have been hurting for a while and companies were unable to pass on the input price increases even as these squeezed corporate margins.

However, WPI inflation remained persistent, with a 30-year high being hit for the FY22 (financial year ending April 2022) at over 13 percent. Even on monthly basis, WPI soared to a 17-year high of 15.08 percent YoY.

The CPI report for April which came in earlier showed prices increasing at their highest pace in eight years at 7.79 percent YoY and 1.34 percent MoM.

With wheat and edible oil prices going up dramatically, it was not surprising that food inflation which holds a 45 percent weight in the CPI basket jumped more than 8 percent YoY. While wheat prices may take a pause post a sudden export ban, edible oils and other food products are unlikely to see moderation, as many of these take their cues from global prices and the Indian Rupee has also been sliding against the US Dollar.

Fuel prices, including both LPG and petrol/ diesel, continue to climb and besides the direct impact on the consumer consumption basket, it will also have a lagged impact via the embedded transport costs in all goods.

While the government has cut duties on fuel in an attempt to cool down inflation, as explained in the next section, this may eventually result in a currency depreciation and hence, another round of imported inflation.

Also, it’s not just food and energy prices that are crushing consumers in India, the core measure (ex-food, fuel & light) itself is running at over 7 percent annually. Clothing, is up 9.5 percent YoY with cotton prices up a massive 123 percent over the last year, plus the price of the petrochem inputs for synthetic textiles is up as well.

Most of the items under Miscellaneous such as Health and Education are running at 7-12 percent annualised rates based on April’s MoM prints.

No wonder the RBI felt the need to front-run the CPI print with an interim rate hike of 40 bps to 4.40 percent along with a 50 bps hike in Cash Reserve Ratio (CRR) to drain out excess liquidity ― a double whammy.

So, now consumers not only have to deal with supply-chain-led price pressures, but also higher interest costs, thus impacting discretionary purchases even further.

Government cuts fuel taxes; bond and maybe the currency markets pay

Before making a hawkish tilt recently, the RBI “pleaded, begged, exhorted” the government for measures like a further cut in excise duty on fuels, but could not manage a response.

As price pressures increased, the government did budge with cuts in duties on fuel plus some cuts in import duties for products like steel, but in a macroeconomic chain this may well provide limited relief to consumers.

The duty cuts will lead to an overextension of an already stretched budget deficit. Over the weekend, news broke that India will probably borrow the entire Rs 1 lakh crore ($12.9 billion) that the government will forgo as revenues. The response was a steepening of the yield curve (short-term yields fell, while long-term yields were marginally higher) on Monday, as market participants expected less aggressive rate hikes if fiscal support comes in.

Unsurprisingly, the Indian rupee dropped to its all-time low against the dollar despite a surprise rate hike and USD selling in the FX market by the RBI to defend the rupee.

In macroeconomics, all variables cannot be managed at the same time. In an effort to contain borrowing costs for the government, the RBI will have to allow the rupee to slide.

This, however, will further fuel inflation, especially for crude oil and downstream products as well as edible oils, where India is heavily import-dependent.

Hence, measures which were meant to cool off inflation may again push up inflation once the effects wind their way through the macroeconomic system.

Now coming to the US inflation trends

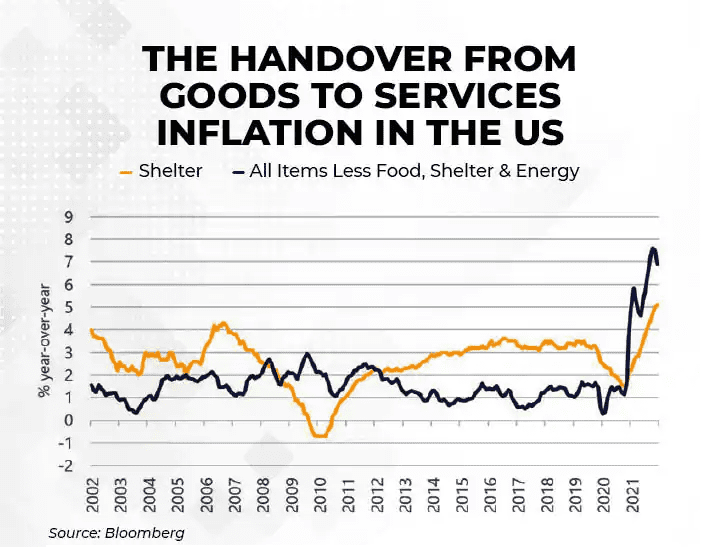

US: The handover from goods to services inflation

While most of the argument around peak inflation is centred around goods inflation receding, as people shift to services on account of re-opening, services inflation is not benign anymore. For example, in the United States, services inflation (ex-food & energy) alone contributed 2.90 percentage points to the 8.26 percent headline inflation number in April 2022.

Shelter, which accounts for 32 percent of the CPI basket in the US, hit 5.1 percent YoY in April and has been rising at 0.5 percent MoM or over 6 percent annualised for the last three months. As mentioned earlier, this was the one inflation component we expected to start moderating, which hasn't happened yet as people hurry to buy homes and lock in mortgages before rates rise even further.

Even if we look at core-inflation ex-shelter, the number stands at 6.89 percent, i.e. more than three times the 2 percent target level ― albeit down from a recent peak of 7.62 percent YoY in February 2022. This suggests that even if goods inflation recedes, services will likely keep inflation numbers high for the near future since the impact of forces like surging mortgage rates/tightening financial conditions tends to operate with a lag.

In short, inflation in the US may prove to be a bit stickier than what we expected earlier.

Core vs non-core: Whose inflation is it?

Central banks, economists and analysts like to look at ‘Core’ inflation, excluding food and fuel which are considered volatile and also less easily targeted by the monetary measures of the Central banks, as the dynamics there are often more supply-led.

But this is economic fiction ― for the consumer these are a core part of her consumption basket. In fact, these are items where she has the least flexibility to make changes, and hence, these crowd out other goods and services if their prices go up. In one sense, what are considered non-core for policy makers are what is absolutely core for the consumer.

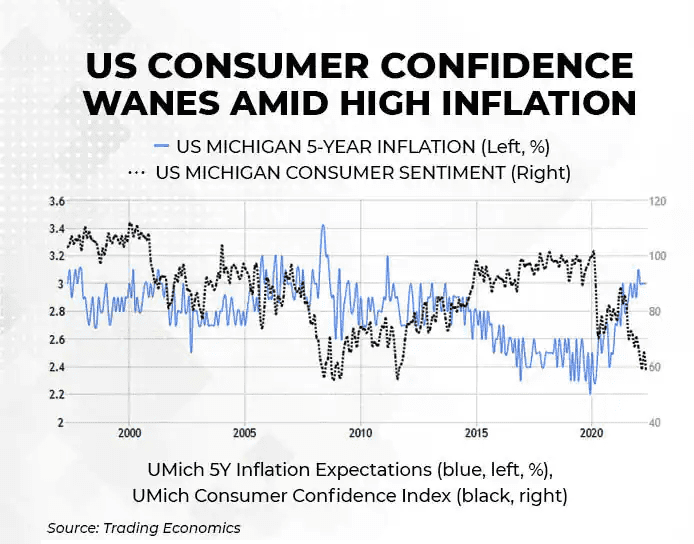

And that also impacts a variable that all of us in the financial markets like to track: inflation expectations.

Food and fuel are exactly the items that consumers look at on a daily basis, thus, influencing their inflation expectations to a greater extent than other items. Plus, consumer confidence goes down too with higher inflation in food and fuel.

As the impact of helicopter money fades in addition to the hike in the prices of goods & services, consumers are bound to cut back on discretionary purchases.

This could explain why there is a disconnect between what the consumer is expecting as against what is expected by the financial markets or financial professionals.

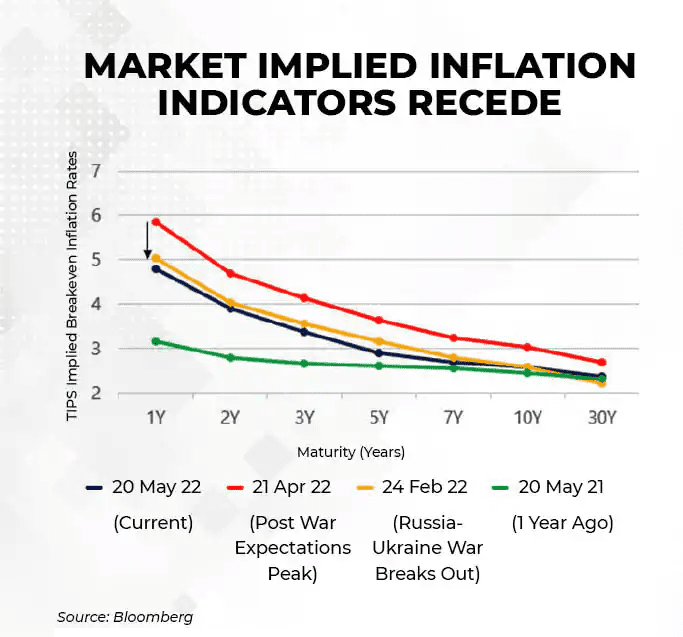

That’s why the University of Michigan's five-year consumer inflation expectations data seems to be stable at 3 percent even as market-implied inflation rates (using treasury inflation protected securities or TIPS) have fallen quite dramatically after peaking in mid-April and are now back to pre-Ukraine invasion (24th Feb, 2022) levels.

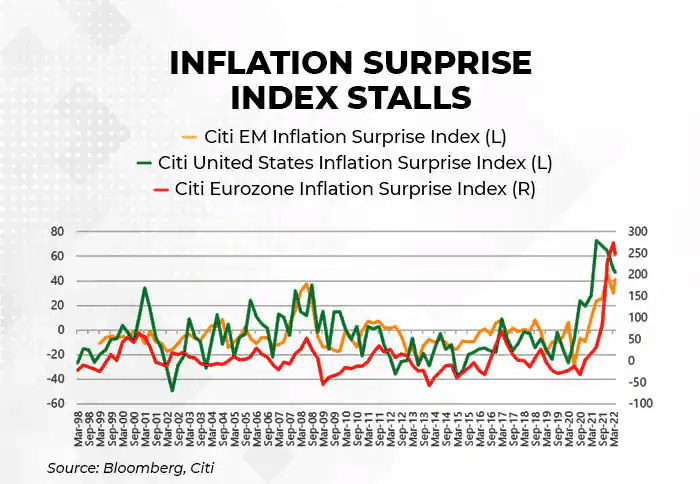

High inflation has ceased to surprise...lately

After calling peak inflation for several quarters as the first graph showed, economists have now come to believe that inflation is not quite so transitory and it has ceased to surprise them.

The Citi Inflation Surprise Indices, which measure the level of actual inflation compared with inflation expectations, have stalled and may possibly be indicating signs of peaking (i.e. CPI prints beating consensus estimates less consistently) in the United States.

However, as Cleveland Fed President Loretta Mester put it, “I will need to see several months of sustained downward monthly readings of inflation before I conclude that inflation has peaked.” Just like in 2021 when the world’s most powerful central bank wanted to see actual CPI prints above 2 percent under the new Flexible Average Inflation Targeting (FAIT) regime, the reverse seems to be true in 2022-23.

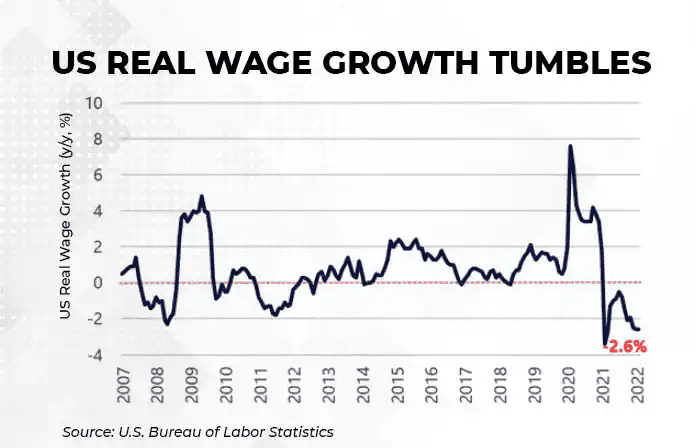

Wage growth runs hot but not in real terms...

One positive in this latest burst of inflation has been rising wages, at least in the US. The employment cost index, a broad gauge of wages and benefits, advanced 1.4 percent in the first quarter of 2022 and rose 4.5 percent YoY, i.e. the most in two decades. Unlike the earnings measures in the monthly jobs report, the ECI is not distorted by employment shifts among occupations or industries.

Even if we do look at the average hourly earnings report, although the growth in the nominal number stood at 5.5 percent YoY, real average hourly earnings have decreased 0.1 percent MoM and 2.6 percent YoY in April.

For sustained consumption growth, sustained real wage growth needs to be positive since most consumers seem to have already drawn upon their pent-up savings and are now taking on more debt, according to Federal Reserve Bank of New York’s quarterly report on household debt and credit.

Looking internationally, inflation of just 2 percent is likely to be sufficient to turn Japanese workers’ real earnings negative. Australians’ real wages are set to shrink as much as 3 percent in 2022 and may only start to catch up by 2024, the Reserve Bank of Australia (RBA) has said.

Meanwhile, in an email to employees on May 5, seen by Bloomberg, Christine Lagarde, President of the European Central Bank (ECB) said she understood that some were “disappointed” by this year’s rise but insisted that future adjustments must be “reasonable.” Elsewhere, central bank workers in Brazil are striking over pay.

...plus the Fed wants to tame the labour market

Fed Chair Jerome Powell laid quite a bit of emphasis on the hot labour market during his May 4 FOMC press conference, citing the need to bring wage inflation down to a level that is more consistent with 2 percent inflation.

Currently, job openings in the US appear to be running at roughly double the number of unemployed people in the labour force.

Even during a recent interview with Marketplace, Chair Powell mentioned that their goal would be to “reduce demand to the point where job openings move down substantially, and the labour market gets much closer to being in balance”. San Francisco Fed’s Daly, who is considered to be a dovish member (non-voting), said during a recent interview, “I would like to see continued tightening of financial conditions ― that would be consistent with bringing supply and demand back into balance.”

Does the ‘Fed Put’ exist amidst tightening financial conditions

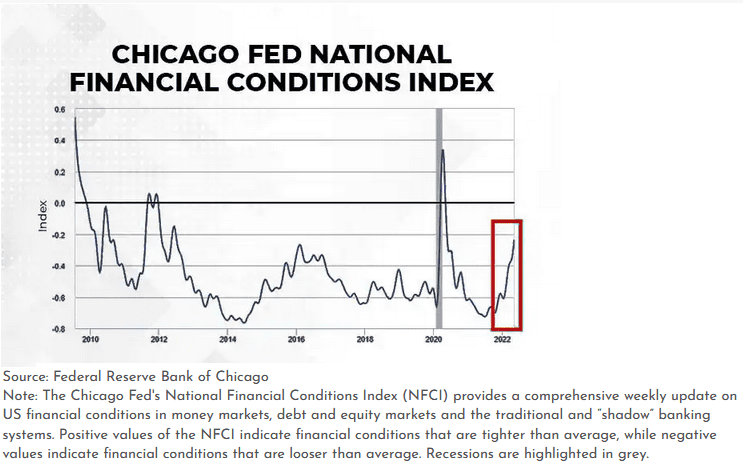

National Financial Conditions Index is getting into the tighter than usual territory, highlighting the rising pressure on risk assets. The question is whether the Fed will be concerned enough to take action and pivot.

In any of the interviews/speeches by the Fed officials there was no mention whatsoever of the large drawdown/ decline in risk assets, particularly in equities. The Fed has made it clear that its current objective is to fight the several decades' high inflation ― everything else can wait.

Also, consider this ― in the US, 10-year real rates (using TIPS) peaked at close to 1.1 percent in 2018 with a core CPI of just 2.1 percent. Today, with a core CPI of 6.2 percent, the real rate stands at a meagre 0.25 percent. This, in our opinion, warrants caution since real rates need to rise while the US dollar index is already trading at its highest level since 2002. With central banks across the world hiking left, right and centre, FX has turned into a race to the top (to reduce the impact of imported inflation) from a race to the bottom we witnessed over the last decade, i.e. a stronger currency has become more desirable.

Instead of looking for the “Fed Put” in equities, one needs to watch credit and funding markets, particularly track the level of credit spreads, velocity of spread widening and accessibility to funding markets. As the saying goes, the market stops panicking when policymakers start panicking.

US high-yield spreads have widened, but still remain 40-50 bps below 2018 levels (when stocks declined 20 percent), meanwhile, due to high energy prices, energy high-yield spreads (391 bps) are below ex-energy spreads (461 bps). Leveraged loan prices have broken 2015 levels in Europe but US leveraged loans are still not close to 2018 levels (getting there).

But then in 2018, managing the inflation was not anywhere close to the top of the Fed's agenda the way it is now. Hence, our bet is the Fed will not care about market moves till inflation is firmly under control.

The Fed’s projection is for ~4 percent YoY inflation by year end, which if missed, is poised to have significant ramifications for risk assets globally. The language from the Fed remains that of data dependence, i.e. prepared to do more (than priced) if things don’t go their way and less if they do.

The answer to the oft repeated question as to what the Fed would do by the end of the year? Even the Fed doesn’t know yet! Depends on what happens to inflation as well as other variables, including the risk of potential recession. It is still about probabilities and fine-tuning as the data comes in.

(A version of this article first appeared in Moneycontrol)

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!