Another article about inflation? Reason to get a bit fed up (pun unintended)? Of course! But there's no getting away from it.

Inflation is currently the tail that's wagging the dog of the entire financial, and for that matter real, world. Inflation is driving policy, especially interest rate policy of central banks plus some fiscal policy (like the duty cuts on fuel in India).

After decades of being a tame, domesticated animal in the developed world, it has come roaring back. Consumer inflation is at a 40-year high in the US and Spain, 48-year high for Germany, 2-3 decades high elsewhere.

And it doesn't look like it's slowing down. In the US, Friday's inflation number of 8.6 per cent year-on-year was 0.3 per cent ahead of the previous one as well as the estimate. Based on month on month data (May 2022 over April 2022), over 70 per cent of items in the CPI basket are now running at an inflation rate of over 4 per cent annualised, up from just 30 per cent a year earlier.

The last time inflation was so high, the Fed Fund rate was in the 13 per cent range. It is 1 per cent now!

While I'm not making the case that the Fed rate is headed to double digits, it can go a lot higher than what was anticipated. The tight labour market is also making reining in inflation expectations more difficult in the US.

More on the relationship between the Fed rate and the US consumer inflation a bit later.

As for Europe the headline inflation is around the same as the US at 8.1 per cent. However, there it is more driven by food and fuel, so while in the US, core inflation (inflation net of food and energy) is at 6 per cent in Europe it is 3.8 per cent.

The dreadful inflation number meant the 2-year US Treasury yields soared 0.55 per cent points in just two trading sessions. The terminal rate expectation i.e. the rate at which markets expect the Fed to end the hiking cycle shot up to 4 per cent.

Since nothing like this has happened in the last three or four decades we have to go back to history to see what the Fed possibly could do.

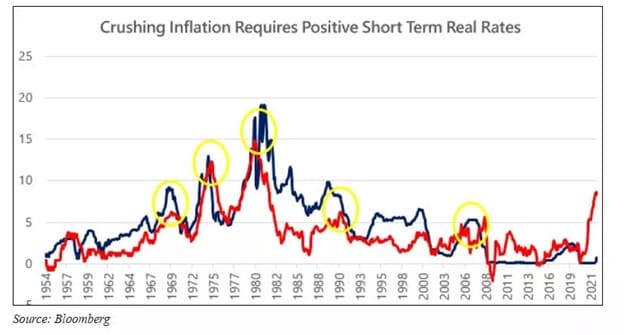

To recap, currently the consumer inflation is running at 8.6 per cent while the Fed rate is 1 per cent this means that the real rate of interest is 1 per cent minus 8.6 per cent that is a negative 7.6 per cent!

Historically, or at least since the 1950s, inflation has never been brought under control without the Fed rate being higher than the inflation rate i.e. without the real rate being positive.

The only exception was during the commodity inflation of 2011-12 which was mainly driven by energy and agricultural product prices. Since it was almost entirely supply driven and also did not exceed 4 per cent in any case, the Fed could afford to sit it out.

This time also the bet was that inflation was supply led and transitory, however that was not the case as there were many other factors also at play, including excess liquidity pumped in by the Fed and the cash handouts.

Even if we remain optimistic and expect headline inflation to drop by half to 4.0 - 4.5 per cent by early 2023, the terminal rate may need to be moved a lot higher in order to have any reasonable chance of controlling the rapid price increases.

The next question is: why do interest rates matter? You can look at the value of a security (share or bond) as the value of all future cash flows accruing to holders which are then discounted at a particular rate. As interest rates go up, this discount rate goes up and hence the value of cash flows received in the future goes down.

Thus, increasing interest rates have a negative impact on the prices of all risk assets, including both equity and fixed income - not to mention the riskiest ones like cryptocurrencies. It leaves few places to hide.

On the other hand, not clamping down on inflation soon enough can result in entrenched inflation expectations and an extended period of inflation and volatility like the 1970s which frankly would be the nightmare (and unlikely) scenario.

The more likely scenario is drastic action by the Fed even if it forces the US economy into recession.

The silver lining? A considerable part of the market correction may have already happened, given that Nasdaq is about the worst performing index in the world year to date.

As an aside, remember my warnings when all those nice sounding NASDAQ ETFs and funds were being launched in 2021? I'd pointed out then that Recency Bias should not blind you to the fact that just because Nasdaq had done well at that point for 2 to 3 years did not mean that it would always do well.

So the inflation, policy, economy and financial markets dance saga continues - we will have to wait for the next installments.

Of course this is all from our narrow perspective of the financial markets. More on the real world impact another time.

(A version of this article first appeared in The Economic Times)

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side as your wealth advisor, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!