.png)

We often speak about our extensive techstack called FG Exotech with a series of subsystems like Turbo™, Glocom™ and Agreement in Motion™ Systems that helps us identify every attractive opportunity in the Global as well as Indian market.

These are a combination of top down and bottom up systems and identify opportunities like the entry into the Metals space in June 2020, Global Marine space in early 2021, Agri and Energy space from Jan 2022 and Exiting China Tech in Feb 2021.

The systems give us an indication to increase exposure to the Indian Capital Goods & Industrial Machinery space, in early October 2021. That's when we started increasing exposure to that space from 8% in October 2021 to 22% currently.

The call worked out beautifully giving us great alpha (ie above market returns) from stocks like CG Power and Industrial Solution, Schaeffler India, Elgi Equipment, SKF India, Cummins etc. to name a few. These gave us returns in the range of 30-300%. Within a span of 10-12 months, some to them went up almost 2-4 times.

Why did our systems like the sector?

Reason One: It was coming out of a long period of sub optimal business conditions as well as below par returns. We always keep a watch for turning points in beaten down sectors.

Capital Goods stocks had a significant run in the 5-year period from 2001 to late 2007, followed by a massive correction by March 2009. Since then, for over a decade, the sector got lost in a secular bear market. Between 2010 and 2020, the sector gave a CAGR of just 2.6% compared to a 9.3% CAGR for the Nifty.

|

|

BSE Capital Goods Index CAGR |

Nifty 500 Index CAGR |

|

Sep 2001-Dec 2007 |

79.0% |

42.6% |

|

Jan 2010-Dec-2020 |

2.6% |

9.3% |

|

Jan 2010-Dec 2021 |

6.1% |

10.9% |

Hence, after being an underperformer for a very long period, plus with more companies as well as the government entering a strong capex cycle, it was possible that the sector will now enter a period of outperformance. Plus, from a valuation standpoint, the sector valuations were quite inexpensive. More on this below.

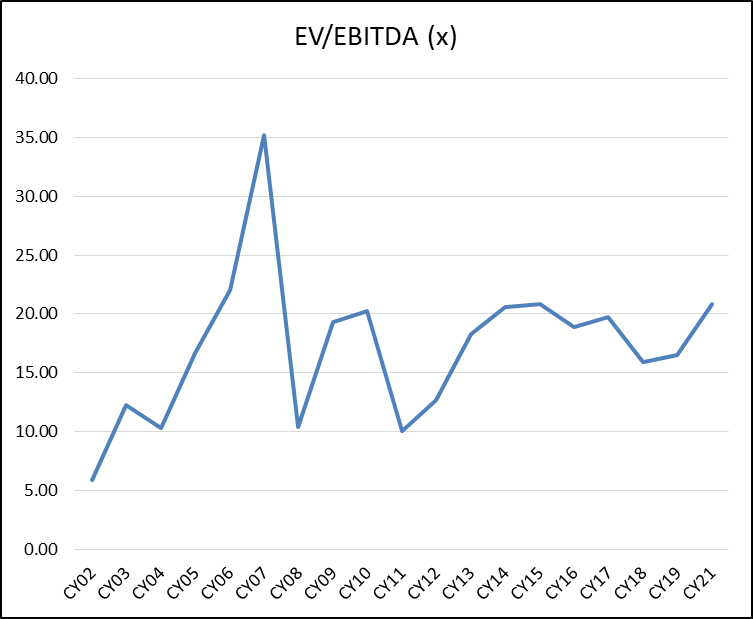

The sector enjoyed peak valuations (P/E of 50x and EV/EBIDTA of 35x) by 2007. Thereafter, valuations fell and again rose up to a P/E of 48x and EV/EBIDTA of 21x by 2015. Thereafter, valuations kept falling year after year and started witnessing a uptick only from 2021. Even, the earnings growth which was a negative 1% and 31% in CY19 and CY20, started showing strong numbers in 2021 and ended CY21 with an earnings growth of 300+%, driving valuations upwards. Our systems were able to catch this up move.

Second, this is inherently a cyclical sector with user industries getting into over capacity situations, cutting back on capex and then after a few years increasing spending once again. With the opening up of the economy since late 2020, the capital goods sector started witnessing strong traction due to healthy order inflows across companies, rising execution levels in key projects, the improving liquidity situation, and spending by the central government.

The Third boost was from the government, both directly and indirectly. The Central government introduced the Production Linked Incentive (PLI) that incentiveised domestic manufacturing.

Plus the 'PM Gati Shakti Master Plan' to create comprehensive infrastructure development plan including roads, power, telecom, etc helped revive the capex cycle, driving further growth in the sector.

A further boost was from global companies making a shift toward a "China plus" strategy to reduce their dependence on that country and India is one of the biggest potential beneficiaries of the shift. This also boosted the capex cycle in certain industries.

Fourth, was the internal work done by the companies in the sector. Most companies in the capital goods space gradually resolved their supply chain and labour issues, improved private corporate balance sheets and improved their capacity utilizations. They were much leaner and once the orders began to flow in, they were in a position to show good profitability.

Lastly, we saw that Capital Goods was a relatively safe haven compared to other sectors which faced margin pressures due to a huge increase in prices of raw materials, coal, electricity , oil and supply constraints plus sluggish demand.

How did this recommendation from our systems do?

Since we started increasing exposure to Capital Goods i.e. from Oct 2021 to August 2022, the BSE Capital Goods index is up 20.8%, as compared to the NIFTY 500 index return of just 1.8% and the stocks we have held are up 2-4 times, adding strong alpha to our portfolios.