The style of investing that has attracted maximum derision in the last decade, it is value investing.

The aftermath of the 2008 crisis in which Central Banks flooded economies and markets with liquidity, effectively crushed the risk-free rate down to levels unseen before.

The effect it had on growth equities was astonishing: the FAANG trade was born roughly one year after the GFC, and did not look back till the end of 2020.

Most investors did not quite understand then, the implications of the effect that a lowering of discount rates has on equities: even a modest lowering of 20% in discount rates can magnify future returns massively. And here we had a lowering of rates by 50% and more!

What essentially happened after the 2008 crisis was that even moderate expected growth became magnified in present value terms simply because of a lowering of discount rates. This, in turn, inflated valuation multiples.

But things have changed a bit lately, due to the hardening of yields, pretty much across the world. This raises discount rates with which to value equities, and this has implications for all sectors.

Does this mean a return of value investing as high flying tech stocks suffer valuations compression because of the higher discount rates that should now get embedded into making valuation forecasts?

It stands to reason that rising discount rates should result in the value space becoming more interesting.

But how exactly should one define value?

The conventional methods are: Low Price-to-Earnings, Low Price-to-Book, high Free Cash Flow Yield, low EV/EBITDA ratios, etc. Their efficacy can be debated but that is not the point of this article.

Is there another lens through which we can define value? We think there is.

How about looking at value in "real” terms, i.e., adjusted for inflation?

We looked at broad sectors globally and compared their real returns with their own past, and also relative to the broader market. We find some interesting patterns here, and we get some insights into what Assets might be considered “value".

Rrelative to the broad S&P Global 1200 Index, sectors such as Energy, Financials, Industrials and REITs are trading in the bottom quintile/deciles of their 25-year percentile return ranges, while the recent high momentum sectors like Information Technology and Consumer Discretionary are within striking distance of their highest levels ever against the broader index since 1995!

When almost all new-economy sectors have delivered strong returns over 10 - 15 years, Energy and Financials have delivered flat or negative real returns in the past 15 years.

In fact, REITs, Financials, Materials and Energy have remained at the lower end even when real returns are sorted by 10 and 15 year timeframes.

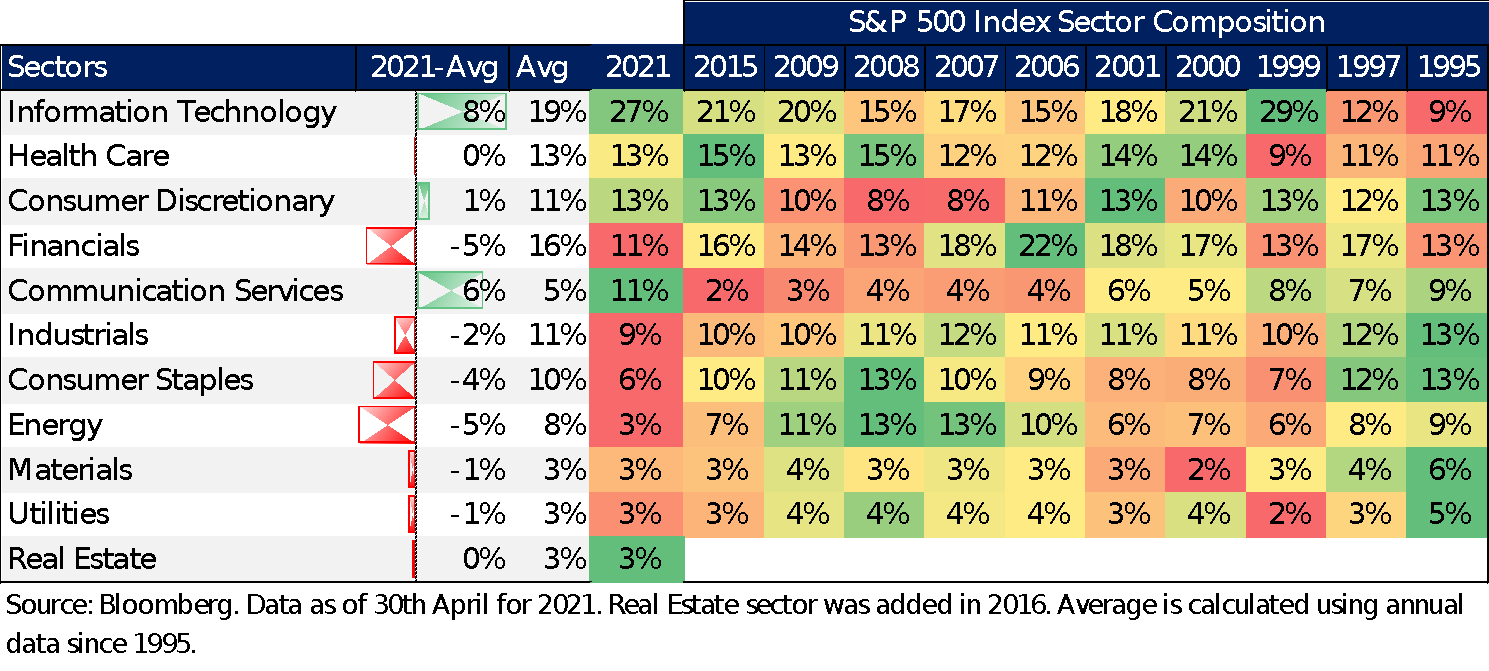

Additionally within the S&P 500, the weightage of these sectors is currently at their lowest level in decades and almost 2 to 5 percentage points below the average weightage over the same timeframe.

Meanwhile, sectors like Technology and Consumer Discretionary have the highest ever allocations in the index (4 to 5 percentage points higher than their long run average).

Just to highlight an interesting data point, the sector exposure of S&P 500 to Technology as of April 2021 is almost 6 percentage points greater than in the year 2000 and just 2 percentage points below its peak in 1999.

The above statistics looked at sectors from a relative value lens, but even on an absolute basis the sectors highlighted above look intriguing.

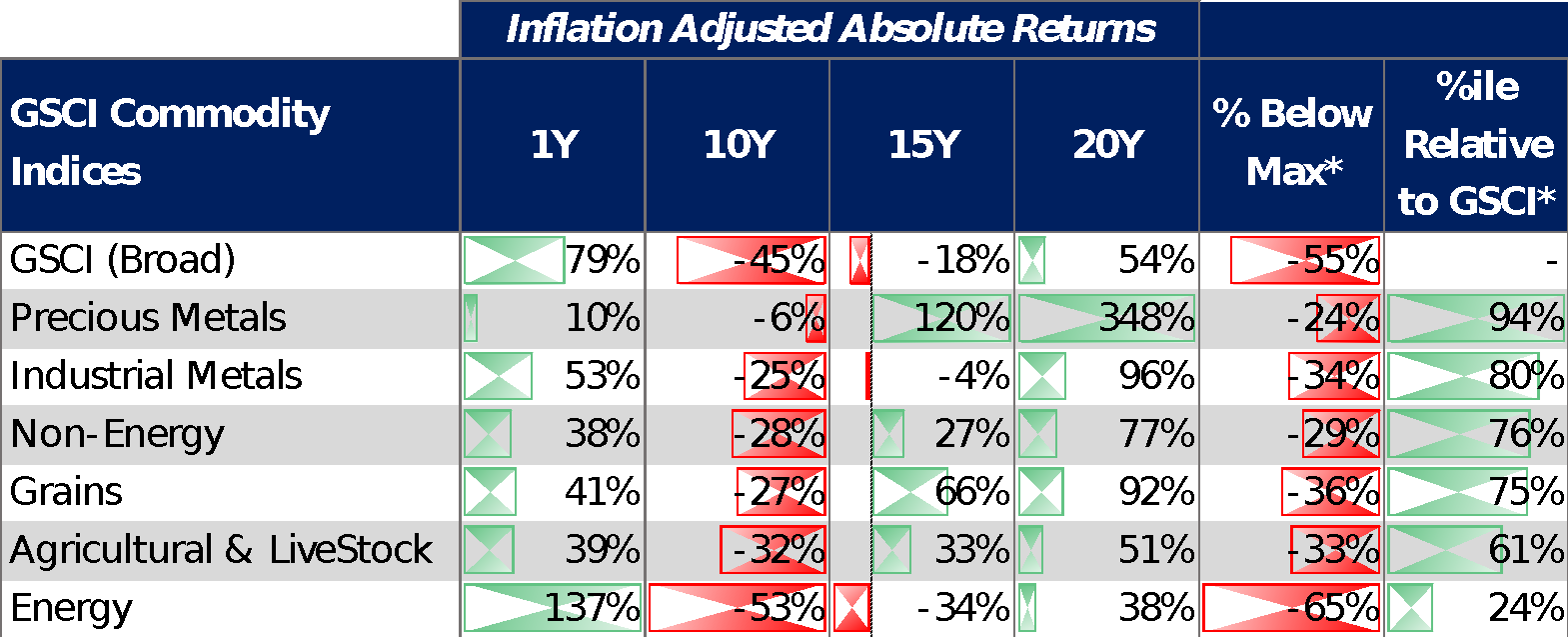

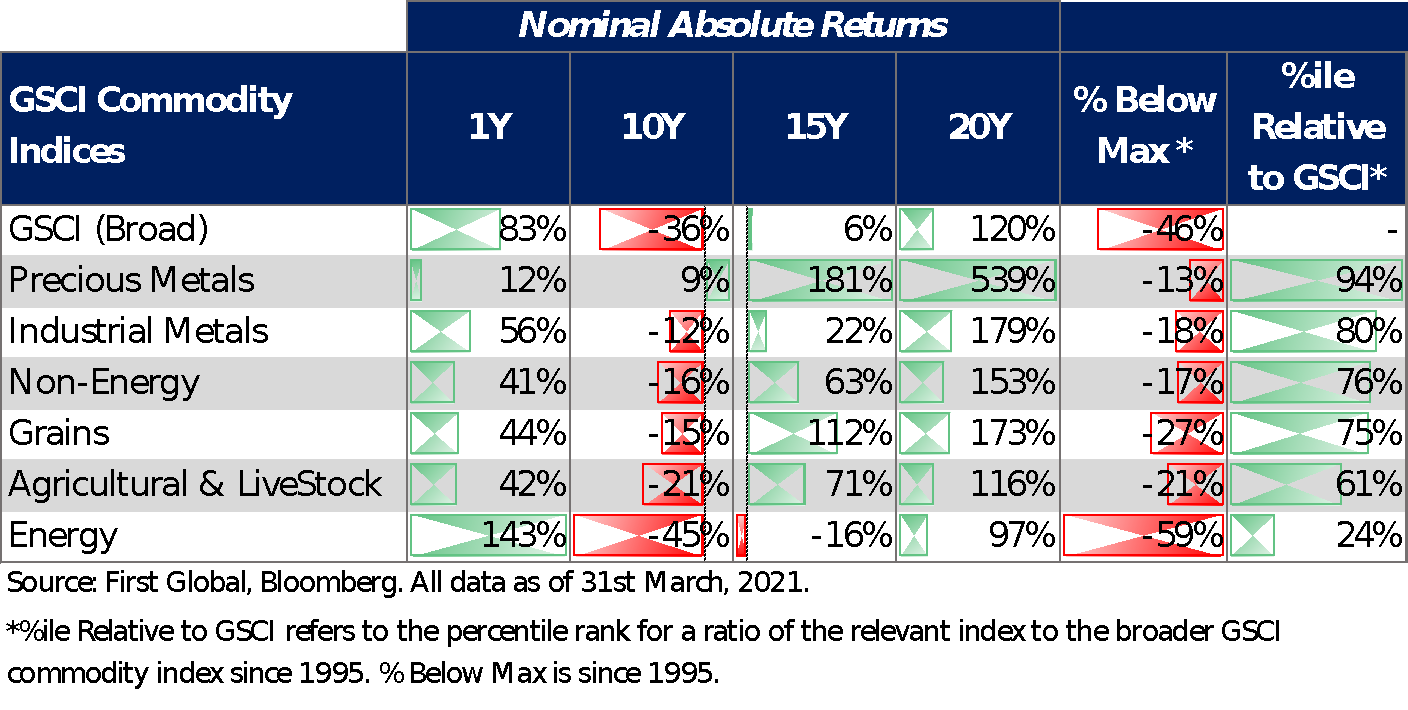

For example, when the broader markets are already climbing to all-time-highs, sectors like Energy (-38%), REITs (-6%) and Financials (-2%), are still trading significantly below their peaks of the past two decades in real terms (in nominal terms as well, in most cases).

Let's think in simple English: Oil today, is the same price as its price in 2005! Copper is at the same price as in 2011 while Aluminum is trading at 2006 price levels.

This means that in real terms, they are lower by at least anything between 20- 40% than their prices of decades ago!

Therefore, this is another way to define value - sectors and asset classes that have "cheapened" dramatically over a decade and more, in real terms.

This list of “Value" is pretty clear: Industrial Commodities. Financials. And from a purely dividend yield perspective, REITs.

These three broad classes represent the deepest value that exists in markets today and they also therefore represent the areas of maximum potential return in an era of rising yields and potentially higher inflation.

Financials

While there are significant disruptions that this sector is undergoing, reality is that even after 13 years of the great financial crisis, the Financials indices have struggled to get past their levels of a decade and a half back, thereby making them extremely cheap in real terms.

Commodities

If one thinks about it, there is hardly anything that we can buy today which was cheaper 10 years back.

Unless of course you're talking industrial commodities!

Even leaving aside crude oil for the moment, hard commodities such as industrial metals, are still trading well below their levels of 10 or even 15 years ago!

The Industrial Metals index itself is down 25% in real terms and 12% in nominal terms over the last 10 years. Many individual metals have fallen even more.

Do physical goods with a related cost of mining/ extraction and refining selling at prices lower than they did 15 years ago, fit the definition of value? Certainly there is a case for thinking so.

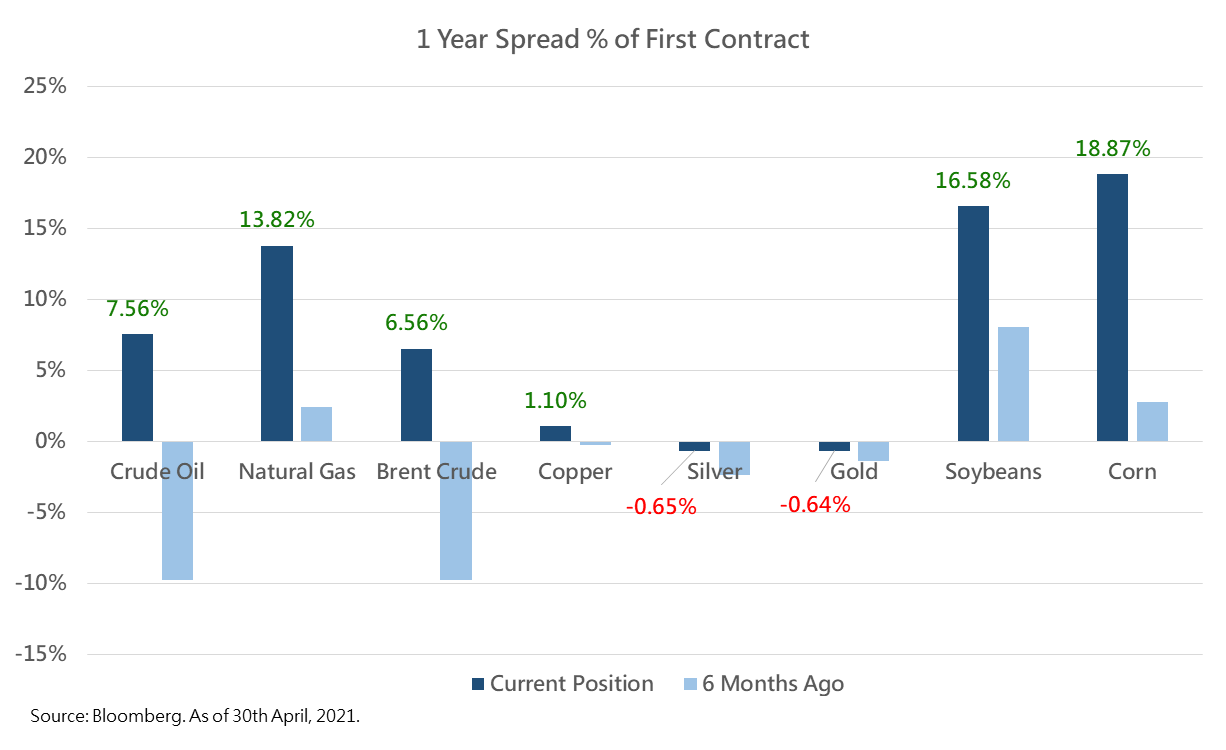

What’s also noticeable right now is that, as of April 2021, supporting the energy market, industrial metals and agricultural commodities in general is also the rising backwardation or roll yield. Over 12 months that process -- known as positive carry -- currently returns 6-7% in oil, 1% in copper, 18% in Corn & 16% in Soybeans, offering a healthy return even before any further price increases. With yields from many of the more conventional asset classes depressed, this is something to be noted.

Real Estate Investment Trusts (REITs)

Then there are REITs, arguably one of the most underappreciated sectors/asset classes.

Let's look at where they are today: They are trading at a significant discount to their all-time highs and also relative to the market.

Even more important, they still provide dividend yields of 4-8% in USD terms - at today's interest rates! Very “cheap" especially for that class of REITs that have not missed their dividend even during the Pandemic turmoil.

In a world of decadall- low interest rates, REITs sure look like value bets based on these metrics.

By altering the lens through which we value “Value”, as we have done above, one can begin to see several asset classes, sectors which are trading at an inflation-adjusted prices much lower than the previous 15 or 20 years'.

Real Estate Investment Trusts, on the other hand, are deep value because of the huge dividend yields that they are paying.

In our worldview, the above are the best "true" value trades available in the world right now which hold potential to beat other sectors and asset classes through the lessening of their long term "cheapness".

(A version of this article first appeared in Business Standard)

From the desk of

Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!