“The Chinese government wants to let a few businesses fail to rein in a bigger problem ... The situation is similar to a controlled detonation. For all practical purposes, a default of Evergrande has already been priced in,” says the Founder of the asset management firm, First Global.

Devina Mehra is one of the sharpest minds in the Indian stock markets. An IIM-A gold medallist and Founder of securities and asset management firm First Global, Mehra had led research at the firm. Her more recent accomplishment is to have built the machine-plus-human approach to investing. First Global is the first Indian securities firm to start tracking US stocks way back in 2001, and Mehra has a keen understanding of global markets, and, yes, when it comes to market predictions, she has several firsts to her credit.

In an exclusive interview with Moneycontrol, Mehra talks about the default of Chinese property developer Evergrande, its impact on the Indian and global market, First Global's top stock and sectoral picks and more.

Q: How big an issue is Evergrande?

A: In our view, the issue is part of a deliberate move by the Chinese government to let a few businesses fail, to rein in a bigger problem. So, they will not let it go out of hand. The situation is similar to a "controlled detonation". In a relatively controlled-economy like China, this is entirely possible. This is in contrast to several somewhat sensational reports and videos floating around.

And for all practical purposes, a default of Evergrande has already been priced in and not just its own bonds - even overall high-yield bonds in China/ Asia have already reacted. So, there's not much further downside there.

Apart from real estate, tech and consumer discretionary, which have also been areas of government crackdown, other parts of the Chinese economy continue to be robust. That is where we are placing our faith.

The primary casualty of the contagion, if any, will be the banking sector. That is a sector we are anyway underweight on.

Q: How much China allocation do you have in your global portfolio?

A: Overall, our exposure to China is just 2.3 percent, well below its representation in the benchmark indices, where the weightage is close to 4 percent. We are in sectors that are more robust -- like clean energy, semiconductors, footwear and chemicals.

We have not taken any direct exposure to the finance and property sectors in China. We also cut out the consumer internet/ tech stocks. A few months ago the government pressure increased in various ways on companies like Alibaba, Tencent, etc.

We will be watching the developments in the chinese market very closely, but one way or the other, it is not going to affect our global fund/ portfolio, materially.

Q: You clearly do not think the Chinese real estate crisis is comparable to the US financial crisis … Like you mentioned, there are some voices comparing it to the Lehman crisis.

A: We don’t think anyone realistically sees Evergrande as a Lehman, but we’ve also seen these periods of China deleveraging weakness before and they aren’t fun. We don’t need the 0.01 percent tail event to be concerned.

However, given the amount of publicity it has already received, property developers and financiers who have already seen credit spreads widen - people are struggling to find even a single bank to sell them a CDS on Evergrande. Effectively, a default risk is already built in, with its bonds trading at 20-30 cents on the dollar.

Q: How do you see this news playing out in the near term? It seems to be impacting sentiment, at least for now…

A: Beijing's focus is on reining in the property sector, which has been highly levered for some time now. But Beijing does not want consumers to suffer. So, the only solution is restructuring and a slow burn in the property sector.

As of June, Evergrande's inventory (consisting of largely unfinished projects) accounted for about 60 percent of its total assets. Properties under development, in particular, ballooned to 1.3 trillion yuan ($202 billion) -- a 54 percent jump from three years ago.

If only Evergrande could offload some of these projects to, say, a cash-rich state-owned enterprise, its immediate liquidity crunch would be resolved. Beijing would then have some breathing room to gradually scale down this beast.

Meanwhile, this would, by extension, impact the construction space and industrial commodities in China. Steel and iron ore are already under pressure due to Beijing's "Blue Skies" mission for winter Olympics. In order to reduce emissions, they're restricting steel production. Iron ore is anyway trading below $100 now. Australian miners can take a big hit and they already are.

Q: What kind of trades are you recommending to investors with a global risk appetite?

A: Our basic stand is always to err on the side of caution and risk-control.

Since we run long-only strategies, even stocks or areas we do not like, we just steer clear of them rather than shorting them.

With that caveat, our view is that if you were to go with the proposition that Chinese banks can blow out in a tail-risk scenario, you're better off betting against Chinese banks/NBFCs with a high exposure to property-related sectors and the least support from the People’s Bank of China (PBOC), i.e., private banks.

We don't think the PBOC will let big banks collapse, considering each of the Big Four banks remain wholly or predominantly state-owned and headquartered in Beijing.

Another possible pessimistic trade is to bet against investment grade names in the real-estate space. The Bloomberg China HY USD index is 66 per cent-real estate. Hence, when you look at the aggregate index, it is mostly a real-estate picture you get.

If you dig into the other parts of the index, the message is quite different, at least for now. It is hard to find big companies outside real estate that have seen significant spread-widening. So far, we think this is a China real estate- specific problem. This is not to say that 'everything is fine'. It is just to be precise about what type of contagion we are observing.

Q: What do you think will be the impact of the Chinese government efforts to rein in Chinese real estate on global commodity demand, supply and prices? Do you think Indian metal stocks, like Tata Steel, have over-run their course?

A: Metals, including steel, had been big winners in our India portfolio from the third quarter of 2020 but we had started trimming these a few months ago.

One reason is that we estimated that the US would try to curb commodity inflation by strengthening the dollar, which actually happened. China has been curbing its own steel consumption for environmental and other reasons.

However, I think the primary impact of this has been and will continue to be on iron ore prices and stocks - especially, Australian miners. Indian steel stocks, while no longer the best bets in the market, don't appear particularly bad either.

Q: What are the key variables you will be watching over the next few days and weeks to see if things may get out of hand?

A: Our systems continue to monitor all macro and market variables for all major economies as well as industry-level data. Like a hare, we remain alert, scanning the environment and ready to change direction if the situation so warrants.

As of now, we are not worried about a contagion from this particular event, but we continue to monitor potential risks and the chinese stock market.

Q: From an Indian market perspective, how do you think the risk-reward is poised for overall markets?

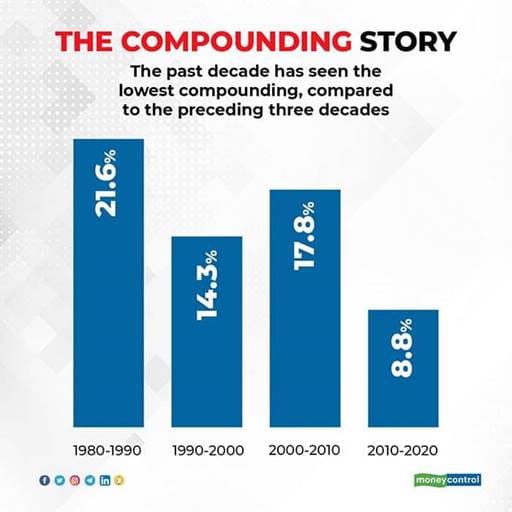

A: Someone recently shared the BSE SENSEX historical data with me, which shows that in the past decade, we have seen the lowest compounding (See chart).

Inherent in these numbers is the risk-reward in the market. Prior to this run, the whole decade gave very sub-normal returns.

As per our Lake of Returns Theory (LORT), returns crash and a bear market comes when the returns have been substantially above trend for a reasonably long time.

As this table shows, we have not had a sustained bull market. Hence, the risk of a sustained bear market is also lower. We have not even come to normal trend returns.

Hence, while corrections can be expected, our systems do not indicate risks of a significant bear market.

Q: Do you think the risk to Indian markets hereon is more local or global? Could you elaborate with data points?

A: We don't think we are through with the pain points in the domestic economy, with recovery still some way away when you benchmark with pre-COVID levels. Consumer distress also remains. To that extent, we are still lagging many other countries.

Globally, for now, COVID-related news remains a risk area. Inflation is not out of hand, at least in the developed world. Hence, the tightening cycle there remains some way away.

Some of the emerging market players, however, have already been tightening. If India does not follow suit -- my bet is that it will not -- currency could be a risk area.

Q: What are your top stock and sectoral picks right now?

A: We have a very diversified basket, with no outsized bets on any single sector. Currently, our relatively higher weights in the India portfolio will be IT, chemicals, cement, and, more recently, telecom. We continue to be underweight on financials as we think the risks there remain relatively high with considerable pain in the Indian and Chinese economy.

From the desk of Devina Mehra

If you want any help at all in your wealth creation journey, in managing your Investments, just drop us a line via this link and we will be right by your side, super quick!

Or WhatsApp us on +91 88501 69753

Chat soon!

Economists Think Dollar's Fall May Explain the Recent ‘Rally’ by Steve Liesman

Einstein taught us about relativity in nature. Now come Devina Mehra and Shankar Sharma of First Global to teach us about relativity in financial markets -- and raise some serious questions about just what is driving stock prices.

First Global reports are quite credible and, on occasion, more than that.

What prompts this mention is Intel's earnings report and the fact that First Global has had a pretty good bead on the company and its stock.

AMD up again following First Global upgrade to ‘buy’ (AMD) By Tomi Kilgore

Analyst Kuldeep Koul at First Global upgraded Advanced Micro Devices (AMD) to "buy" from "outperform," given the "exceptional traction" that the chipmaker's Opteron line of processors has been able to get.

Baidu Climbs on First Global’s ‘Outperform’ Outlook

Baidu Inc., the operator of China’s most-used Internet search engine, rose to the highest price in two weeks after First Global rated the shares “outperform? in new coverage.

Personality counts: Walmart's frugal, but Target charms

"It's better to take a slight hit on [profit] margins and keep on moving and inventing," says First Global Securities. And at least for now, Target is inventing in a way that appeals to consumers with money to spend.

Dead Batteries

At 11 times trailing earnings, Energizer is cheaper; Gillette's multiple is 25. But cheaper doesn't mean better, says First Global.

Bipinchandra Dugam @bipinchandra90

@devinamehra @firtglobalsec

invested in both GFF-GTS and Super I50. Thank you very much for such wonderful investing experience with completely new approach. In my 15years of investing first product I felt which close to what customer want.

Shishir Kapadia @shishirkapadia1

@firstglobalsec @devinamehra

by far you are the best, I have not come across transparency, acumen, global expertise, exposure, protection of capital, delivering return from any fund/ fund managers. Invested very small size in 3 products will keep on increasing it over the period

Piyush Bhargava @PiyushB88762654

@devinamehra @firstglobalsec

Thanks you team FG specially Devina, my investment doubled in less than 3 years in SDPB As a investors & PMS distributor of your product looking to have a long-term relationship with the company.

@KarmathNaveen the person with whom I always interact

Sumeet Goel @GoelSumeet

Very happy & relaxed to be invested with first global pms

Shishir Kapadia@shishirkapadia1

Congratulations on super performance, above all transparency and systematic process are unmatchable.

One must opt this, if person consider him/her self as an investor. Very happy to be part of this since invested. FG has managed worst year (ie 2022) so efficiently and skillfully.

SY @SachinY95185924

With so much of volatility in the market, risk management is very important part & considering that FG is doing awesome work!!! Kudos to you Chief

Amit Shukla @amitTalksHere

Truly outstanding. As a retail subscriber to #fghum #smallcase, I can vouch for the Nifty beating returns (8% vs 3%) in last 1 year. Keep up the awesome work @firstglobalsec

We can load above testimonials on site as a scroller, and just below that we can add a section for compliments . Below tweets are comments and praises are related to our content, performance and some our direct compliments to you.

ADIT PATEL @ADITPAT11226924

Good team...

Special mention @KarmathNaveen .. he is soo helpful anytime of the day or night..

Hindustani @highmettle

Bought Peace with FG-Hum.Moving all funds from DIY investing to well managed and diversified PF at low cost.

It has doubled almost, excellent pick.Every small investor must invest in her FG-HUM Smallcase.

Suresh Nair @Suresh_Nair_23

I have 8 small cases and your has been the most rewarding ones .. thank you Devina.

Sayed Masood @SayedM375

There is absolutely no doubt that she is one of the best investors of India in modern times but more importantly, she shares the most sincere and sane advice with retail investors.

SY @SachinY95185924

Wow Superb Returns🔥 Congratulations Chief for being Number 1 among all PMS!!!

You are one of the sharpest mind in Global Stock Market

AnupamM @moitraanupam

Congratulations Devina, results talk in itself!

Abhishek @simplyabhi21

Congratulations ma’am @devinamehra ! The consistency you have in maintaining the top rank position is outstanding! 👏

Mihir Shah @Mihir41Shah

We are learning More about markets (& Life ) thanks to U than we learnt in our Professional courses.A BIg Thank You, Wish all get Teachers Like You!!

Sumit Sharma @MediaSumit

"The ability to be comfortable with being outside consensus is a superpower in investing...and in life." Devina ji hits the nail on its head!

Majid Ahamed @MajidAhamed1

Congratulations @devinamehra mam! All the best for long term returns as well.

Vinay Kumar @VinayKu05949123

This is the wonderful session I have ever attended till date. One of the most fruitful hour of my life. Devina madam, ur clarity on financial mkts is simply superb.The way u portray the facts supported by "data" about stock mkts is really astonishing.I will listen again.Thanks.

VIJAY @drippingashes

I loved to read your journey, insight and philosophy. It's a pleasure to read and know of your takes on market and life.

MNC🏹 @Focus_SME

Check & follow @devinamehra's timeline for lots of post debunking such rosy stories. Also, she gives amazing 🤩 sector directions/hints.

KLN Murthy @KLNMurthy2016

Good actionable insights, great article!

Suresh Nair @gkumarsuresh

Devina Madam is simply terrific... good knowledge, straight and simple thinking.

Very difficult to emulate such traits. I listen her past interviews from youtube.

Respect...!!!!

DD @AliensDelight

One of the brightest minds in the world of finance :)

Radhakrishnan Chonat @RCxNair

📣 Calling all investors! Just had an incredible interview with @devinamehra, Chairperson and MD of First Global. We discussed the importance of global diversification, effective asset allocation, and the risks of sitting on the sidelines. Trust me, you don't want to miss this!

siddarthmohta @siddarthmohta

Excellent performance. Flexibility is the key as you have mentioned it earlier also. Cannot have finite rules for infinite mkt opportunities.

Boom (বুম)@Booombaastic

To be honest, the insights which Devina madam brings in is very enriching..have learnt a lot from them...

Himanssh Kukreja @Himansh02428907

One of the most accurate analysts :)

I always look forward to you interviews mam

Abhijeet Deshpande @AbhijeetD2018

Madam, It is always a treat to read your insight, not only on business but on other topics also!!

Dada.AI @dada_on_twit

Thanks for this wisdom ma'am. Always love hearing your thoughts on everything equity. :-)

adil @zinndadil

Excellent points!

Can clearly feel this thread is a product of marination of many books and years of experience. 👍

Kamal thakur @Kamalgt10

Superb !!

Your knowledge, analysis & articulation is simply great 👍

Tanay @Tanay36232730

Follower on Twitter and Subsciber on YouTube of First Global, really helping me in my investment desicion. Thanks

Copyright 2019, All Rights Reserved. Developed By : Hvantage Technologies Inc. Maintain By : Aarav Infotech